The US Federal Reserve is often pressured to ease or pivot away from tighter monetary policies, as investors and the general public tend to prefer “easy money” or accommodating monetary conditions. High and rising interest rates can constrain economic activity, increase the cost of capital, and lead to sell-offs in long-duration assets such as growth equities, long-term bonds, and real estate.

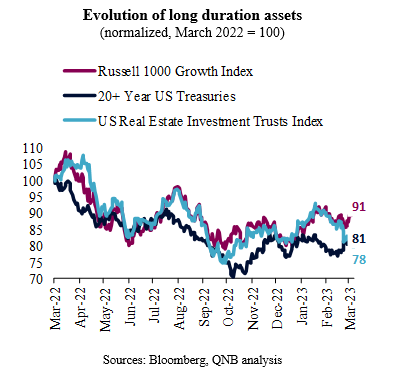

Since March last year, in response to significantly above-target inflation, the Fed implemented one of the most dramatic and unexpected monetary tightening cycles in US history. This resulted in negative surprises and marked declines in growth stocks (-9%), long-term Treasury bonds (-19%), and US real estate assets (-22%). These declines underscore the need for closer examination of the Fed’s monetary policy and their impact on financial stability.

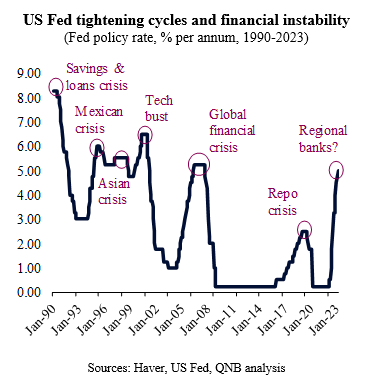

As a natural part of the tightening cycle, more restrictive financial conditions can create negative wealth effects. However, the process can sometimes result in severe unintended consequences, particularly when market movements become disorderly, leading to financial instability, credit crunches, and sharp economic downturns. In fact, major financial crisis over the past several decades have often developed during periods of high and rising interest rates.

In recent weeks, the first signs of financial instability started to come to the fore. US regional banks with large unrealized losses on their bond portfolios witnessed large deposit outflows. This lack of confidence led to rapid bank runs on more vulnerable institutions, such as California-based Silicon Valley Bank and New York-based Signature Bank. Fears of contagion then emerged, and economic authorities had to intervene to make deposits whole and create a new liquidity window. The announced Bank Term Funding Program (BFTP) allows banks to post Treasuries and other government debt at par with the Fed, enabling lenders to avoid distress sales and honour deposits.

Financial instability heightened the debate about whether the Fed is ready to “pause” or even pivot the policy rate changes sooner rather than later. Lower inflation expectations and weaker growth prospects are now driving investors to believe that the Fed will cut rates in the second half of the year. Fed fund futures are signalling 100 basis points (bps) of policy rate cuts by January 2024.

However, during the last meeting of the Federal Open Market Committee (FOMC) in late March, Fed officials decided to increase rates by another 25 bps. Importantly, Jerome Powell, Chairman of the Fed, clearly communicated that the inflation mandate remains a priority and rates are expected to increase further.

In our view, rates are set to remain higher for longer. We expect one more 25 bps hike in May for a terminal Fed funds rate of 5.25%. In addition, we do not expect any rate cuts until at least 2024, despite the ongoing unease about financial instability.

Two factors underpin our view, as we keep in mind that the Fed’s formal monetary policy framework targets an average 2% inflation rate.

First, despite a significant pullback in inflation in recent months, from 9.1% in June 2022 to 6% in February 2023, conditions are still not in place for the Fed to meet its target. Irrespective of the ongoing economic slowdown, US labour markets are still the tightest in decades and the current 5-6% wage growth needs to moderate sharply before inflation consolidates at levels that are more appropriate. It is therefore important for the Fed to keep things tight so that the labour market can gradually ease.

Second, the fine-tuning of different monetary policy levers creates room for the Fed to maintain a tight stance against inflation while managing financial stability risks. We believe that the tension between the two objectives is likely to lead to a “decoupling” of monetary policy tools. In the past, most central bankers supported the need for an alignment of policy tools, i.e., policy rates and balance sheet should be pointing to the same direction or at least not contradicting each other – easing, neutral or tightening. This led to the playbook of combining policy rate hikes with balance sheet stability or reduction, in contrast to balance sheet expansion, which increases money supply and liquidity in the system.

Over the last few weeks, the Fed has further emphasized a differentiated approach in the application of monetary policy tools: interest rate policy as the main tool to combat high inflation while balance sheet policy will be adjusted, in a targeted matter, to potentially backstop stressed financial markets. This allows for a more orderly and sustainable process of monetary policy adjustment.

Download the PDF version of this weekly commentary in English or عربي