The Euro area economy contracted sharply in 2020 due to the outbreak of the pandemic, but has experienced a strong recovery in 2021. Average growth reached 5.5% on a year-on-year (y-o-y) basis in the first three quarters of 2021, mainly driven by the effects of fiscal stimulus, re-opening of the economy and rollout of vaccines. While the economic outlook remains positive, risks to growth tilts to the downside in the short-to-medium term.

This analysis delves into the three risks to the outlook for economic growth in the Euro area over the next few quarters: a resurgence in Covid-19 cases, rising inflation and global supply constraints.

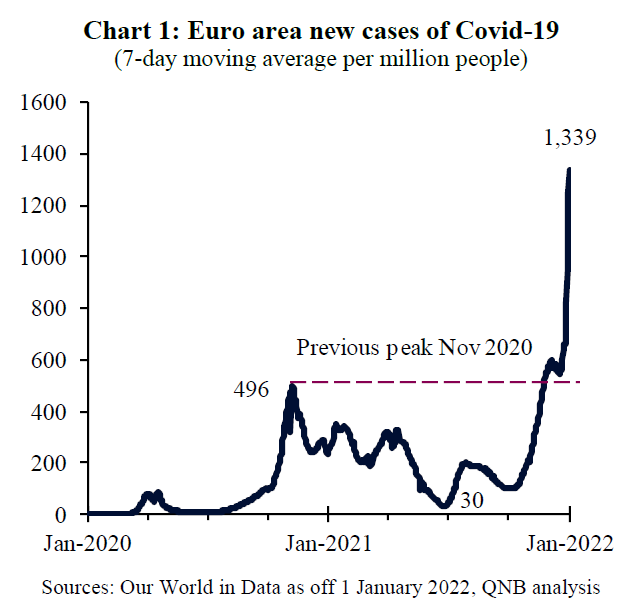

First, the resurgence in new cases is forcing several governments to tighten their coronavirus rules. The number of new cases of Covid-19 in the Euro area has already reached nearly three times as high as the previous peak in November 2020 (Chart 1). This is mainly because the new Omicron variant, which has a particularly large number of mutations, reduces vaccine efficiency against mild infections. As a result, many Euro area countries have reintroduced various forms of travel restrictions and lockdowns. For example, the Netherlands has introduced stricter local lockdown measures, Germany and France are banning travellers from the UK, and Italy requires pre-departure tests for all tourists from the European Union (EU). Tighter restrictions will significantly reduce economic activity in the services sector (bars, restaurants etc.) during what would normally be a busy time of year during the festive season.

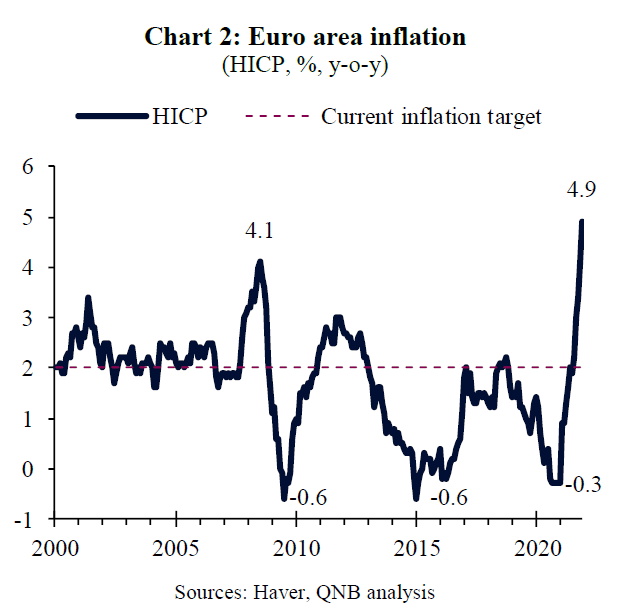

Second, the rise in inflation, driven mainly by high energy prices, is a risk to the outlook for economic growth. Consumer prices (CPI) rose rapidly in 2021, reaching 4.9% y-o-y in November, the highest level since the introduction of the Euro in 1999 (Chart 2). The rise in CPI reduces the purchasing power of people’s wages and other income, dampening consumer spending. Should high inflation be persistent, the European Central Bank (ECB) will come under increasing pressure to tighten monetary policy earlier than currently expected. Tighter monetary policy, by reducing the size of asset purchases or eventually raising interest rates, would slow economic growth via lower availability of credit to consumers and businesses for investment.

Third, global supply constraints are a headwind for activity in the Euro area manufacturing sector. For example, supply chain bottlenecks are contributing to higher input costs and longer delivery times. This has contributed to the manufacturing Purchasing Managers Index (PMI) falling from peak of 63.4 in June to 58 in December 2021. If supply chain bottlenecks are more persistent than we expect, then they will limit economic activity in the Euro area and are therefore a downside risk for the outlook.

All in all, a resurgence in new cases of Covid-19, persistently high inflation and more persistent global supply constraints are risks to the economic outlook. Countries with lower levels of vaccination, tighter labour markets and larger manufacturing sectors are more vulnerable to these risks.

These risks, together with slowdowns in both the Chinese and US economies, mean that we see the outlook for economic growth in the Euro area to be weaker than forecast by the International Monetary Fund in their October World Economic Outlook (5.0% in 2021 and 4.3% in 2022).

Download the PDF version of this weekly commentary in English or عربي