“We are all Keynesians now.” That was notoriously stressed by US president Richard Nixon in 1971, months before engineering the end of the USD convertibility into gold and launching fresh new measures to accommodate large government spending. The famous quote, referring to John Maynard Keynes’ prescriptions of government spending to stimulate demand during cyclical downturns, is a testament to the central role of macroeconomics in determining the perceived performance of elected officials. Whenever an economic crisis threatens to disturb private demand, creating unemployment, even fiscal conservatives such as Nixon turn to “big government.”

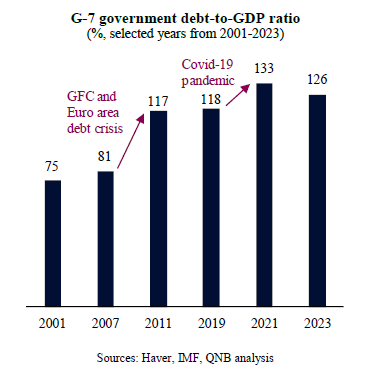

Importantly, however, over time, there is a strong tendency for government debt to accumulate. In fact, G-7 countries’ (Canada, France, Germany, Italy, Japan, the UK, and the US) government debt as a percentage of GDP has expanded from 75% to 126% in less than a generation from the beginning of the new millennium. Debt accumulation tended to accelerate following periods of crisis, such as the Global Financial Crisis (GFC) of 2008-09, the Euro area debt crisis of 2010-11 and the Covid-19 pandemic in 2020.

While the level of indebtedness has contracted a touch since the peak of the pandemic, this is more a function of a strong economic recovery and abnormally high inflation rates than any significant effort of fiscal consolidation. In our view, fiscal conditions are likely to deteriorate further across most of the G-7 countries. Three main factors support our position.

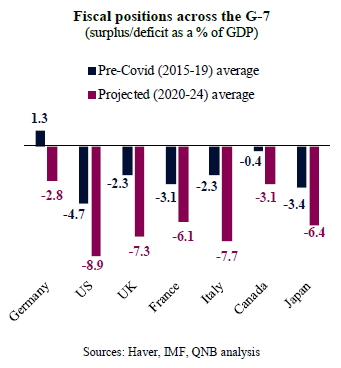

First, all G-7 countries have widened their deficits since the pandemic, irrespective of the post-pandemic recovery. Even Germany, which pre-pandemic was the only country with structural surpluses within the G-7, became a deficit country in recent years. This comes as a plethora of new bottom up demands increases pressure for further government spending. Such demands include social entitlements, geopolitical pressures and the needs for a new Capex cycle to upgrade infrastructure as well as to promote strategic industrial sectors. The result is a more constant requirement for further government spending that cannot be easily funded by new taxes, given the overall high level of taxation across most of the G-7 and the impact of higher taxes on competitiveness.

Second, after a period of aggressive monetary tightening following the post-pandemic surge in inflation, policy rates are significantly higher than long-term nominal GDP growth in all G-7 countries except for Japan. This suggest a significant potential for fiscal de-anchoring due to unsustainable debt dynamics, with a further increase in debt-to-GDP ratios. Hence, in the absence of a significant cycle of policy rate cuts by the US Federal Reserve, the European Central Bank, the Bank of England and the Bank of Canada, the fiscal position can worsen rapidly.

Third, the Covid-19 pandemic “legitimized” the use of an unconventional policy mix often referred to as fiscal-monetary coordination or indirect debt monetization, which raises the ceiling for government indebtedness. In normal circumstances, the combination of elevated indebtedness with wider fiscal deficits would produce large spikes in long-term bond yields, tightening financial conditions and placing disciplinary pressure on governments. However, in order to prevent and supress financial distress, central banks are now expected to intervene and support the government bond market should yields go up too much or too fast. On the other hand, this allows government to enact more excessive fiscal policies. As a result, fiscal authorities have less market constraints on them, which enables wider fiscal deficits for longer across most of the G-7 countries.

All in all, while there are no major crises in sight to require a step change in indebtedness levels across the G-7, fiscal conditions are set to deteriorate on the back of a high demand for more government spending, high nominal policy rates and the deployment of fiscal-monetary coordination.

Download the PDF version of this weekly commentary in

English

or

عربي