Despite a challenging global macro environment, driven by factors such as high inflation, tighter monetary conditions, and geopolitical frictions, emerging markets (EM) are set to benefit from a more positive 2023. As the year progresses, market participants have been increasingly recognizing the resilience and opportunity of several EM economies.

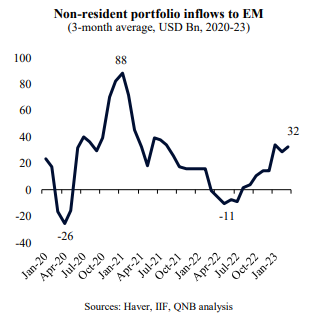

According to the Institute of International Finance (IIF), non-resident portfolio inflows to EM, which represent investments from foreign investors into local public assets, experienced a significant shift. After a period of negative or tepid figures throughout much of 2022, these inflows increased to a three-month average of more than USD 30 Bn. This influx of capital has contributed to significant gains across EM asset classes, including over 17% in total return for equities (MSCI EM) and 14% for bonds (J.P. Morgan EMBI Global) from their recent lows.

Amid a challenging global macro environment, what drives the optimism surrounding certain EM? In our view, there are two key factors that explain the increasingly positive backdrop within the EM space: the reversal of USD overvaluation and stronger macroeconomic fundamentals in most EM compared to advanced economies.

First, the USD overvaluation is in the process of reversing, which is a powerful tailwind to EM assets. As a classical “safe haven” play, the USD tends to be negatively correlated to most “risk on” assets, including EM equities and bonds, which are considered even riskier than similar assets from more stable, advanced economies.

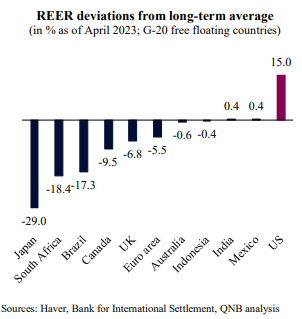

The USD has already depreciated by almost 5% against major EM currencies since late last year. Importantly, despite the moderation of the USD strength in recent months, the USD real effective exchange rate (REER) – a trade-weighted, inflation-adjusted FX rate – continues to point to a 15% overvaluation of the US currency against its long-term trend. The REER is often used to determine the “fair value” of different currencies, as it captures changes in trade patterns between countries as well as economic imbalances in the form of inflation and inflation differentials.

Further adjustments of the USD over the coming quarters are likely to push capital outside of the US towards other economies, as a weaker USD favours global diversified portfolios. This should be particularly beneficial for advanced economies that have undervalued currencies, such as Japan, Canada, the UK, the Euro area, and Australia. However, EM with floating undervalued currencies are also set to benefit, including South Africa and Brazil. In fact, a general diversification away from the USD is expected to lift all countries, including other EM.

Second, macroeconomic fundamentals are currently stronger in most EM than in advanced economies. Several advanced economies have been accumulating acute imbalances from excessive policy stimulus following the pandemic and the Russo-Ukrainian War, leading to issues such as high public debt and inflationary pressures. This was due to the need to protect the income of households and corporates from large negative shocks.

In contrast, most EM countries had less policy space to adjust to the pandemic shock. Furthermore, EM central banks in countries with a history of chronic inflation, such as Brazil and Mexico, faced pressure to pre-emptively implement interest rate hikes early in the inflation cycle. This proactive approach was crucial in preventing inflation from spiralling out of control and maintaining macroeconomic stability.

As a result, EM countries are now under less pressure to tighten policy and may even start early easing cycles, as their economies have already largely adjusted to less benign global conditions.

All in all, global capital flows have begun to return to EM, driven by the ongoing reversal of USD overvaluation and comparatively stronger economic fundamentals in most EM countries. Additionally, institutional investors are lightly positioned in EM assets. A new quest for more investment diversification, driven by factors such as high valuations in developed markets and concerns over inflation, could trump the prevailing sentiment that favours US assets as the “only game in town.” Currently, institutional investors hold less than 10% of their equity portfolio in EM, against an MSCI EM benchmark of 12% and the fact that 34% of total global revenues are derived from EM. Any meaningful change in allocation policies can create significant further global capital inflows to EM.

Download the PDF version of this weekly commentary in English or عربي