There is no doubt that expectations for 2024 were influenced by the experience of investor sentiment from 2023, when negative initial expectations were countered by positive macro surprises. In fact, Bloomberg consensus forecasts for global growth ended up increasing significantly by 80 basis points (bps) throughout 2023, from a “recessionary” 2.1% in January to a more palatable 2.9% in December.

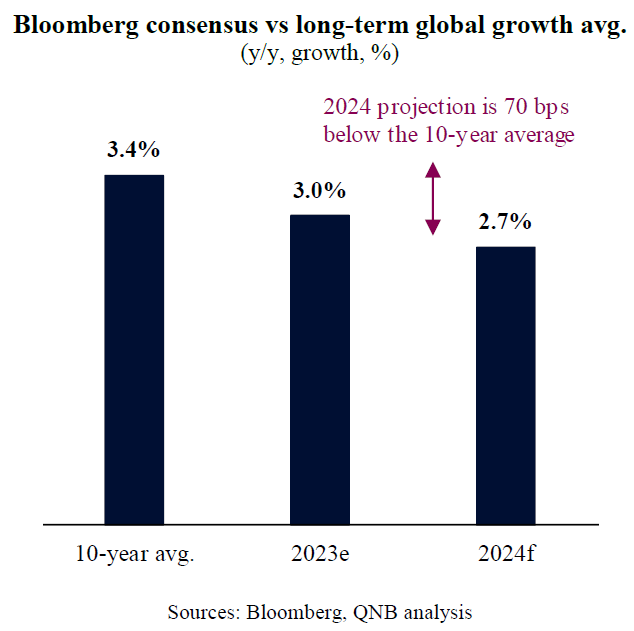

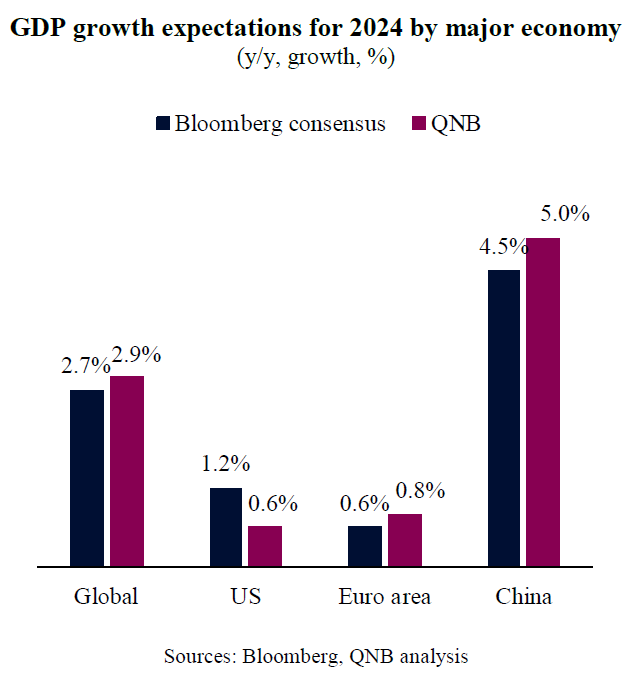

As a result, this year, analysts are more cautious with their forecasts. Bloomberg consensus forecasts currently point to a weak if still positive expansion of 2.7% in 2024. This implies a moderation from last year, maintaining global growth markedly below the 3.4% long-term average.

Entering into 2024, our own view is slightly more bullish than consensus, as we see the global economy expanding by 2.9%, roughly the same rate as last year. However, while our aggregate view is not materially different from consensus, our projections are meaningfully different on a major economy or regional basis.

On the negative side, our expectations for growth in the US are very different from what is embedded into the consensus. While most analysts expect the US to achieve a smooth “soft landing,” where growth gently slows, we project a deeper economic downturn. In our view, the US economy should grow by 0.6% in 2024, significantly less than the 1.2% projected by the poll of Bloomberg forecasters and the 2% average long-term growth. Our view even implies a “short, shallow” US recession in H1 2024.

Our weaker US view is predicated in three main points. First, the US economy is already slowing rapidly. After an extraordinary GDP growth of 4.9% annualized in Q3 2023, the Atlanta Federal Reserve nowcast estimates a growth of only 2.0% for Q4. This rare sudden deceleration suggests a rapid adjustment to a less benign macro environment. Second, after a period of ebullience, investments are falling sharply, with capital expenditure intentions now nearing negative territory. This is led by a retrenchment from the private sector on the back of higher debt costs. Third, fiscal policy in the US is quickly turning from a tailwind into a headwind. The US fiscal thrust, which measures the net contribution of government budget policies into growth, is set to decelerate from a positive 1.9% in 2023 to a negative 1.4% in 2024. Hence, the US economy should slow down more than most analysts currently expect.

On the positive side, however, we expect the Euro area and China to outperform consensus projections. In the Euro area, despite the ongoing stagnation, predicated on tight financial conditions, weak external demand, and lasting energy vulnerability, there is scope for modest improvements. We believe inflation will return to target more rapidly than currently expected, allowing for earlier and deeper rate cuts by the European Central Bank (ECB). Moreover, the Euro area should benefit from a moderate recovery from the recent “global manufacturing recession,” that weigh negatively on major European exporters. A rapidly falling inflation amid relatively strong labor markets should also produce real income gains, potentially boosting discretionary consumption. Therefore, we expect to see a modest, but above consensus growth of 0.8% in the Euro area in 2024, still weak versus a long-term average of 1.4%.

In China, following a period of expansion after its late post-pandemic “reopening,” the economy lost momentum again on the back of weak real estate and low consumer confidence. Deflation started to take hold as households seem to be determined to save more. Importantly, the government aims for a more balanced growth strategy, favouring long-term stability and national security rather than the aggressive policy stimulus packages of the past. Fiscal and monetary stimulus are expected to be limited but firm, calibrated to sustain a normal level of activity rather than investment booms. There is significant policy room for state agencies to stimulate and prevent a more significant slowdown, even with all the existing challenges. Microeconomic reforms are set to continue and gradually improve business sentiment, bringing back the “animal spirits” that were hit by the regulatory tightening from 2022. Finally, the country should also benefit from the global manufacturing recovery. As a result, we expect moderate growth of around 5% for China in 2024, below the long-term average of 6.2%.

All in all, the global economy is set to remain lacklustre in 2024, growing below its long-term average. All the three main economies (the US, Euro area and China) are expected to grow slower than their long-term averages. When it comes to performance vis-à-vis consensus expectations, however, there seems to be too much “optimism” about US growth and “pessimism” about Euro area and China growth.

Download the PDF version of this weekly commentary in

English

or

عربي