Historically, particularly over the so-called “Great Moderation” period (1990-2019) dominated by positive growth and low inflation, there was rarely too much interest into actual inflation prints. Stable macro conditions allowed for inflation to be reliably projected several quarters in advance. In recent years, however, following the shocks from the pandemic and the Russo-Ukrainian conflict, high inflation returned, with price pressures becoming not only more pronounced but also more volatile and difficult to predict. Hence, unsurprisingly, the inflation debate emerged as the most important point of the US macro agenda.

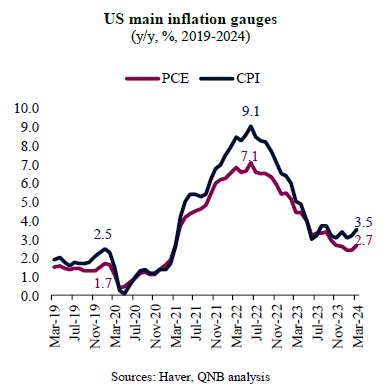

US inflation, measured by both the personal consumption expenditure index (PCE) and consumer price index (CPI), accelerated quickly amid the post-pandemic recovery, before reaching a multi-decade high in June 2022. This produced significant macro instability and required several rounds of aggressive monetary policy tightening by the US Federal Reserve (Fed). Subsequently, after mid-2022, inflation moderated markedly, getting closer to the 2% Fed target. This was driven by supply chain normalization, a healthy economic slowdown and tighter monetary policy.

A rapid inflation slowdown spurred optimism amongst monetary authorities and investors, leading the Fed to change its forward guidance with the communication of potential rate cuts ahead.

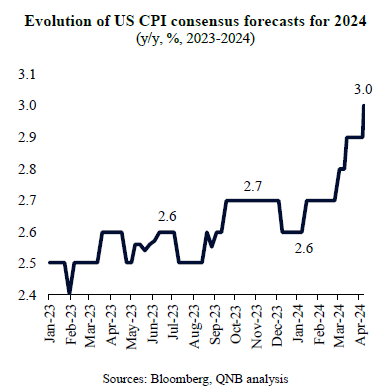

However, the optimistic take on inflation has been challenged in recent weeks, as the official price prints for January, February and March 2024 were higher than previously anticipated. As a result, market confidence in a rapid inflation conversion to the 2% target has been waning. This suggests that there could be a struggle to erode the “last mile” of above-target inflation. In fact, Bloomberg consensus forecasts point to a rising 2024 median inflation projection to 3% in the US. Importantly, consensus forecasts also imply that inflation is not going to return to target until 2026.

On the back of these recent negative developments, Fed officials have been reassuring markets that policymakers can take their time before they start enacting rate cuts, in order to insure that the downward trend for inflation is not in danger. According to Chairman Jerome Powell, “the recent data have clearly not given us greater confidence and instead indicate that it is likely to take longer than expected to achieve that confidence.”

In our view, despite recent signs of sticky price pressures, there are reasons to be less pessimistic about US inflation over the near and mid-term. We expect inflation to moderate further over the coming months, with the main inflation gauges converging towards their target earlier than most analysts anticipate. Three main points support our view.

First, leading indicators for inflation point to a further continuation of the downward trend towards the Fed target. The producer price inflation (PPI), which has been leading headline inflation by around a quarter, has decreased rapidly, reaching 2.1% in March 2024. This is due to a normalization of supply chains, as the effects of the re-opening of the economy and the Russo-Ukrainian conflict stabilized, with global input prices weakening. In addition, PCE inflation, the favorite price gauge used by Fed officials, have already slowed to close to target and remain on a dowtrend. This suggests a significant moderation in overall price pressures.

Second, despite recent volatility in headline inflation, the long-term trend of non-cyclical inflation remains benign, suggesting a return to “normal” 2% inflation sooner rather than later. The components of inflation that are not overly sensitive to the business cycle have moved lower for over two years, recently re-entering the 0-2% range that prevailed before the pandemic.

Third, the labour market is losing momentum, which should prevent wage growth from advancing too much over the coming months. While unemployment rates remain low, forward looking indicators for the labor market are now less robust. This can be observed alongside two dimensions: the quits rate and job creation figures. A key indicator that showcases employees willingness to take risks and voluntarily change jobs, the quits rate is pointing to a deterioration in labour market confidence, as around 12% less people voluntarily quit their jobs in February 2024 versus the previous year. Job creation has also weakened significantly, indicating a more difficult backdrop for wage negotiations. The cost of labour is key for services as well as cyclical inflation. This should further offset wage growth, helping to limit price pressures.

All in all, we expect inflation to close the “last mile” more rapidly than what is currently implied in consensus expectations. This is due to positive signs from leading indicators, a meaningful downtrend in non-cyclical inflation and a weakening labour market. This should allow the Fed to cautiously move ahead with rate cuts in H2 2024, as current policy rates are too high for both the existing and expected levels of inflation. However, even with the expected rate cuts indicated by the Fed for the year, interest rates should remain “higher for longer,” i.e., are not expected to return to the negative real levels experienced after the Global Financial Crisis and before the post-pandemic recovery.

Download the PDF version of this weekly commentary in

English

or

عربي