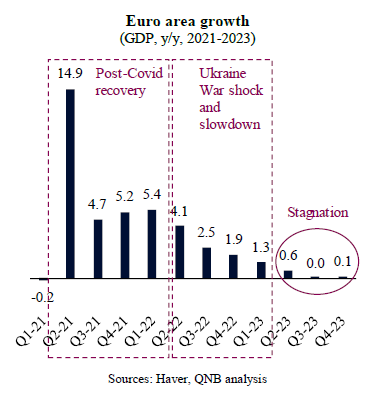

The Euro area has been in a negative spiral since early 2022, when the region was caught in a doom loop of geopolitical uncertainty, high energy prices, record monetary tightening, and weak external demand. As a result, the post-Covid economic recovery was followed by a significant slowdown on the back of the Russo-Ukrainian conflict. With a deeper energy crisis avoided by good weather, fiscal support and strong tourism seasons, the economic blow was softened.

While the Euro area as a whole was able to avoid a recession so far, there seems to be no end in sight for such potential threat. Out of the 20 member countries of the Euro area, nine are officially in or very close to a recession, including Germany, the Netherlands and Austria. Importantly, headwinds are still looming over the region and the economy is in a standstill for three quarters now, broadly stagnant even as other advanced economies, such as the US, presented a more robust performance with some re-acceleration.

Moreover, analysts and economists are projecting further weakness ahead, with the Bloomberg consensus pointing to a tepid 0.5% growth in 2024, far below the long-term average growth of 1.4% for the Euro area.

Obviously there is little room to be excessively optimistic about growth in the Euro area, as the lagging effects of restrictive monetary policy still need to take place and fiscal policy accommodation should be gradually withdrawn. However, we do see some room for positive surprises, which justifies our above consensus forecast for 0.8% growth in the Euro area. Three main factors underpin our view.

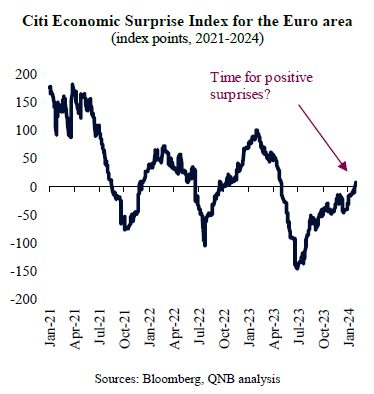

First, the flurry of negative economic data surprises in the Euro area seems to be exhausting itself, pointing to some extreme pessimism that is likely to produce positive surprises in the near future. This is reflected by the recent moves in the Citi Economic Surprise Index, a timely figure that measures the pace at which economic indicators are coming in above or below consensus forecasts. For the first time in more than nine months, data has been mostly producing positive surprises since early February 2024. These types of turns tend to imply that projections are currently too gloomy and should start to be revised upwards.

Second, lower and falling inflation is expected to produce real income gains, potentially boosting discretionary consumption. In fact, inflation has been collapsing in the Euro area, from a peak of 10.7% in October 2022 to 2.9% in December 2023, with leading indicators suggesting a more rapid convergence towards the 2% inflation target of the European Central Bank. This, in a context where wage growth is still strong, running above 5% per year, point to real income gains that are likely to be translated into higher household spending. As consumption makes up for more than 73% of the Euro area’s GDP, this may be a powerful tailwind for stronger growth.

Third, manufacturing is expected to be more supportive for Euro area growth over the coming months. After an unusually deep and long “global manufacturing recession,” which has been in place since 2022, a positive turn towards an expansion cycle is expected. The Global Manufacturing Purchasing Manager’s Index (PMI), a timely indicator of whether activity is improving or deteriorating, has bottomed in July last year and improved thereafter. The latest print, from January 2024, point to activity at the brink of turning expansionary. An expansion manufacturing cycle often gains momentum rapidly and lasts for about 1.5 years. This is expected to be supportive for the Euro area, as manufacturing represents 15-20% of the region’s GDP.

All in all, while we do not expect strong growth for the Euro area this year, we believe consensus figures are too negative. Positive macro data surprises, real income gains and a more supportive global manufacturing cycle should prevent a deepening of the ongoing economic stagnation in the Euro area.

Download the PDF version of this weekly commentary in

English

or

عربي