U.S. inflation is at present one of the most closely monitored macroeconomic variables globally. Over the last several months, higher than expected price pressures have created concerns of inflation being stickier. If sustained over time, such pressures could jeopardise the Federal Reserve Board’s plan to start easing their monetary policy stance this year. This is why it is important to take a closer look at key inflation gauges.

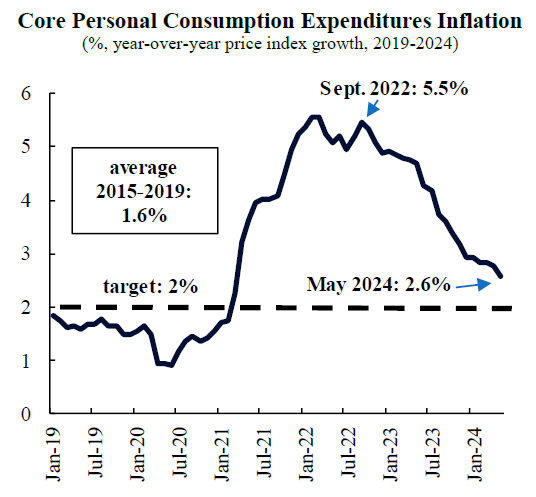

The preferred price measure for the Federal Reserve is the index of prices from Personal Consumption Expenditures (PCE). The “core” version of the PCE price index strips out more volatile goods, such as food and energy, which are sensitive to external factors, such as weather shocks and geopolitical events. By removing prices that are more susceptible to short-term volatility, it provides a more informative indicator of underlying inflation trends. According to the PCE-core measure, inflation peaked in 2022 amid the post-Covid pandemic recovery. Since then, inflation has moderated markedly, driven by supply chain normalization, a healthy economic slowdown, and tighter monetary policy.

In our view, although progress could be uneven, inflation will continue to converge towards the target of monetary policy, allowing policy makers to begin the next rate cutting cycle in September this year. In this article we discuss the three main factors that sustain our outlook for inflation.

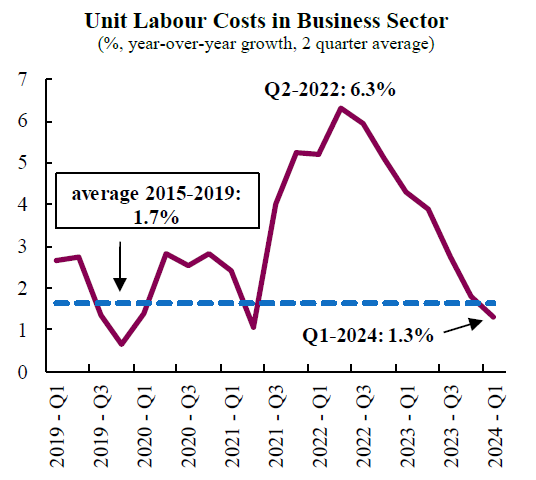

First, strong productivity growth in the U.S. will contribute to bring inflation back to its target. Increasing productivity means that more goods and services can be produced with a given level of resources, reducing costs of production, and therefore leading to lower prices for consumers. During the 1990s, for example, advances in information technology, and of the internet in particular, were a driving force behind the acceleration in productivity growth in the U.S. In turn, increased efficiency and competition contributed to keep inflation under control.

In the three quarters ending in Q1-2024, output per hour in the nonfarm business sector increased at an average rate of 2.7% in year-over-year terms, far outperforming productivity growth in other advanced economies. On the back of strong productivity growth, unit labour costs have continued to descend markedly since their peak of 6.3% in Q2-2022 towards the pre-Covid pandemic average below 2% of 2015-2019, contributing to the moderation in inflation.

Second, cooling labour markets are set to soften the demands for higher wages by workers, reducing pressure on labour costs for firms. While the unemployment rate stands at an historically low level of 4.1%, indicators that tend to anticipate conditions in labour markets are signalling that the labour market is losing momentum. The rate at which workers quit their jobs is falling, a trend that reveals that workers are less confident in their ability to find new jobs or successfully search for better conditions in a new position. Similarly, the number of job openings continues on a downward trend that started at the beginning of 2022. Given the importance of labour costs for the production of services and goods, a weakening labour market will contribute to contain price pressures.

Third, decreasing inflation in the housing component of prices will become a key contributor to falling total inflation in the coming quarters. Housing represents approximately 15% of the PCE index, and includes either rent or, if the housing unit is owner-occupied, what it would cost to rent an equivalent unit in the current housing market. Inflation in housing reached a peak of 8.2% in April 2023, much later than the peak in overall inflation, which reflects the “stickiness” or rigidity of prices in this segment, where longer term contracts determine costs and therefore prices react more slowly to changing macroeconomic conditions. Rents can only change when a lease expires, which typically occurs annually. Housing inflation has fallen at a steady pace since mid-2023 and is currently below 6% in year-over-year terms. However, market indices of newly contracted rents, which anticipate the trends in the traditional statistic, show that rent inflation is below pre-pandemic levels. This signals that the housing component of prices will continue to decelerate during 2024-2025 helping to bring overall inflation down.

All in all, inflation in the U.S. has come down significantly from its peak and should continue to moderate over the coming months towards more acceptable levels, on the back of strong productivity growth, falling labour market pressure, and decelerating rent inflation. This will set the stage for the beginning of the cycle of interest rate reductions by the Federal Reserve in September. We expect two 25 bps cuts this year and subsequent 25 bps cuts every other policy meeting until early 2026, when rates should rest at 3.75-4%.

Download the PDF version of this weekly commentary in

English

or

عربي