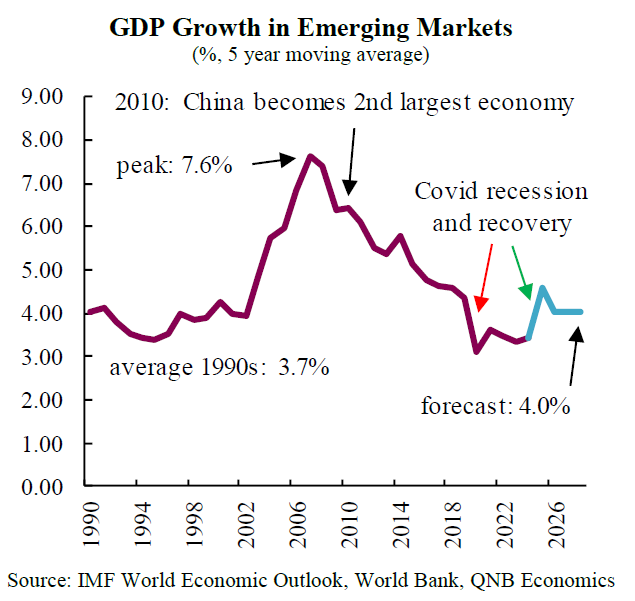

Emerging markets (EM) have been a driver of global economic growth for many years. EM, defined as the group of countries that are in the process of rapid economic development, grew at rates that were three percentage points higher than those of the advanced economies for over two decades. In fact, growth in EM accelerated sharply in the early 2000s from 5-year average rates that were below 4%, to a peak of 7.6% in 2007. Beneath these impressive aggregate figures, numerous examples showed that a country could sustain a rapid pace of development and catch-up to advanced economies if appropriate measures through policies and reforms are taken.

The ascent of the Chinese economy accounted for an important part of this aggregate development, both directly and indirectly. Directly, given China’s significant weight in EM and growth rates of near 10% for several decades. Indirectly, as the effect on other economies materialised through supply-chain linkages, the demand for imported commodities, and a growing influence in international investment flows.

However, the exceptional performance of EM began to lose strength after the Global Financial Crisis (GFC) in 2007-2008, and later faced significant volatility during the Covid-pandemic and the subsequent recovery. Importantly, we expect that growth will converge to more moderate rates of around 4% until 2030. In this article, we analyse four main factors that will weigh on EM performance going forward.

First, investment growth of capital in EM is expected to fall below the average rates of the last two decades. Previous periods of strong investment growth were supported by robust credit expansion, capital flows, improvements in terms of trade (prices of exports relative to imports), and reforms aimed to enhance the investment climate. During 2000-2010 investment growth in EM averaged 9.4%, but then dropped to 4.8% during 2011-2021. This slowdown was extensive across all the EM regions and explained by factors including worsening terms of trade, elevated debt levels, higher economic and geopolitical uncertainty, and China’s rebalancing towards consumption and away from investment and exports. Importantly, we expect this trend to persist. Given the critical role of capital accumulation for growth, the slowdown in investment points to a major headwind in the coming years.

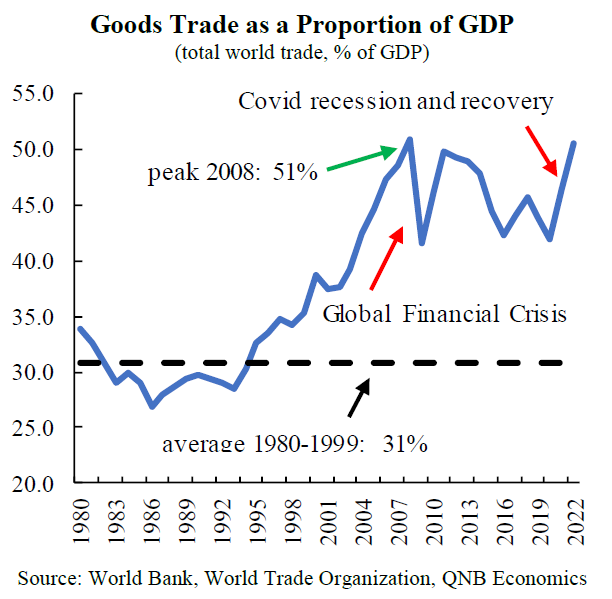

Second, historically, international trade has been one of the pillars of global economic perfomance, given its positive impact on output and productivity growth. The process of global integration was boosted by regional trade agreements, multilateral negotiations, and unilateral trade reforms. As a result, trade in goods as a share of global GDP reached unprecedented levels in 2008. Nevertheless, trade has stalled over the last decade driven by a trend towards de-globalization, which limits the margin for trade to give additional support to growth. Tariff reduction was an important driver of trade expansion previously, but now tariffs are already low on average in both advanced and emerging economies. Additionally, structural factors, such as the rebalancing of economies towards services, will naturally reduce the weight of trade in the economy. This process will weaken the role of goods trade as a growth engine in coming years.

Third, the Chinese economy is undergoing a significant deceleration relative to its performance in previous decades, diminishing its role as a global growth driver. After 40 years of soaring growth rates averaging 9.5% during 1980-2019, this pace is likely to fall below 5% on average. The slowdown is driven by numerous structural factors including demographic headwinds, declining productivity growth, high debt levels, a slower pace of structural reforms, and the rising threat of geo-economic fragmentation. Given the importance of the Chinese economy for EM growth through direct and indirect channels, the slowdown in China implies an important challenge in the coming years.

Finally, the broad-based slowdown in productivity growth in EM is expected to continue, adding another drag to economic growth. According to estimates by the World Bank, productivity in EM grew at an average rate of 2.2% in the period 2000-2010, and decelerated to 1.6% in 2011-2021. This trend will further consolidate, with average productivity growth declining to 1.4% during 2022-2030. The slowdown in productivity growth is due to various factors, including the deceleration in working-age population and educational attainment growth, and a smaller productivity gap with advanced economies which implies a weaker “catch-up” process. Furthermore, the extent to which EM will be able to leverage artificial intelligence to reverse the decline in productivity growth is highly uncertain.

All in all, after two decades of exceptional performance, growth in EM will continue to moderate in the coming years, given significant headwinds from weakening productivity and investment growth, the long-run deceleration of the Chinese economy, and stagnating global trade. This raises the bar for the structural reforms needed by developing countries to continue their process of catch-up to advanced economies.

Download the PDF version of this weekly commentary in English or عربي