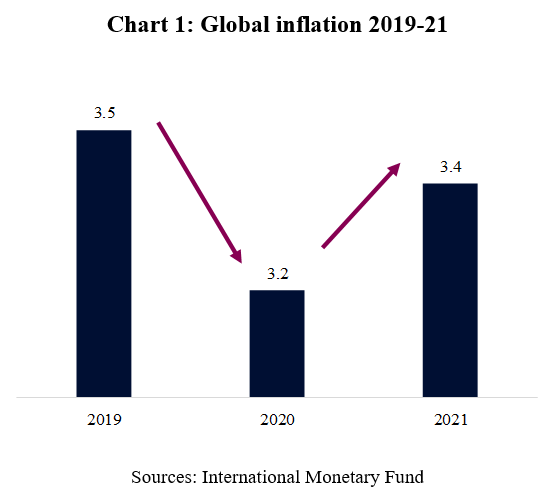

Inflation in advanced economies has been stubbornly low ever since the 2008 global financial crisis (GFC). Then, last spring, the Covid-19 pandemic hit the global economy and lockdowns caused a collapse in economic activity. This led to a sharp fall in oil demand and energy prices. The pandemic also hit consumer demand across the world. Together these factors resulted in lower global inflation in 2020. Now, these factors which dragged inflation lower in 2020 are either reversing or were temporarily leading to higher inflation in 2021.

Too little inflation is a bad thing, but too much inflation is also a bad thing. Indeed, a key objective for central banks is to achieve price stability. Inflation targeting became popular as an anchor for monetary policy in the early 1990s. The UK central bank adopted inflation targeting in 1992, followed by the European Central Bank in 1999. But, it was not until 2012 that the US central bank (the Fed) adopted an explicit inflation target, even though it maintained a dual mandate to also target maximum employment.

Central banks responded to the pandemic with massive policy stimulus using interest rate cuts, asset purchases and liquidity injections to support the economy. Governments also responded with significant fiscal stimulus. Further, the rapid development of effective vaccines offers hope for continued recovery to a new normal.

Three main factors are putting upward pressure on inflation in 2021, higher energy prices, the expiry of some economic support measures and increased shipping costs. It is important to remember that inflation is defined as the year-on-year change in the level of prices, which means that a one-off change in prices simply falls out of inflation after 12 months.

First, higher energy prices. Oil prices fell sharply last spring, dragging down on inflation throughout 2020. Oil prices have now recovered to around the same level they were before the pandemic, so will soon begin to push up on inflation as they begin to be compared to the low level of prices last year.

Second, temporary Covid-19 economic support measures will boost inflation in 2021. For example, a number of European countries (including both Germany and the UK) cut VAT temporarily last year, which lowered the level of consumer prices and pulled down inflation in 2020. But, as VAT returns to normal this year, there will be a symmetric impact, pushing inflation up in 2021. Another example is, higher Medicare payments to doctors in the US, as part of the Covid-19 stimulus package, which are effectively a temporary increase in prices that will increase inflation in 2021.

Third, increased shipping costs for consumer goods. Global shipping costs, as measured by the Freightos Baltic Index, which is based on the cost of shipping containers, has almost trebled since the start of last year. The pandemic induced a shift in consumption patterns as lockdown diverted expenditure from services to consumer goods. This has resulted in a surge in demand for containers and shipping services to move them from areas of production (mainly Asia) to areas of consumption (the US and Europe).

These temporary factors are expected to push up inflation over the first half of this year. Indeed, all major forecasters that we follow expect higher inflation in 2021. Before the GFC, such a surge in inflation would have set alarm bells ringing. But today, central banks will welcome a period of higher inflation because it has been stubbornly low since the GFC. Indeed, we expect central banks to effectively “look through” the temporary factors pushing inflation up in 2021 and focus on maintaining as much support for the economic recovery as possible.

In conclusion, inflation will pick up noticeably over the next few months and remain elevated throughout most of 2021. However, modestly higher inflation is actually a positive indicator of the ongoing recovery in the global economy. Indeed, the temporary nature of the factors pushing up inflation in 2021, combined with spare capacity in both product and labour markets, make it unlikely that inflation will increase further and become a real concern in the near future.

Download the PDF version of this weekly commentary in English or عربي