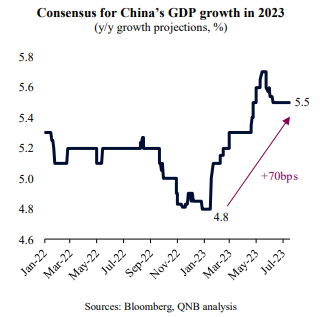

Early in the year, China was one of the main reasons for our higher than consensus view on global growth for 2023. Negative narratives from investors and analysts dominated the agenda, as the Bloomberg consensus forecasts pointed to a slow 4.8% Chinese recovery from a weak 2022. The Bloomberg consensus is a tool that tracks global forecasts from economists, think tanks and research houses, presenting a range of projections as well as the median point of market expectations.

Lower growth expectations were following a period of sequential negative headwinds, such as new waves of Covid, rolling lockdowns in major cities, a real estate crisis, lacklustre policy support, and private sector uncertainty associated with aggressive regulatory clampdowns on innovative companies. However, despite all the headwinds from 2022, we were expecting to see a more robust cyclical recovery in China this year, as the country was preparing to pivot away from ultra-restrictive healthcare and economic policy measures.

It did not take long for China to undertake those pivots, starting the so-called “economic re-opening.” As a result, since the beginning of the year, growth consensus forecasts for China grew by 70 basis points to 5.5%. Despite continued weakness in manufacturing, service consumption boomed to even surpass its pre-pandemic trend. After seven months, we maintain our 5.5% growth projection for China in 2023.

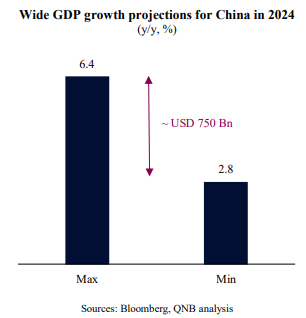

Moving forward, however, as the economic re-opening is behind us, the scenario is much more uncertain. A good reflection of this uncertainty is the wide discrepancy between the maximum and minimum (max-min) forecasts for China’s growth in 2024: the most optimistic forecaster expects 6.4% growth, while the most pessimistic forecaster points to only 2.8% growth. The difference is key, not only for China but for the entire global economy. Should the more bullish forecast prove to be right, China will add around USD 1.3 trillion to the global economy. In contrast, should the bearish scenario materialize, China would only add USD 542 billion. The gap between the two outcomes, amounting to USD 750 billion, is what separates the GDP of a relatively large country like Spain from a smaller country like Austria.

In our view, both China “bears” and “bulls” are likely to be disappointed, as we expect the country to maintain a moderate growth rate of around 5% next year. Two main factors support our view.

First, “bearish” or more pessimistic analysts are likely to be disappointed because manufacturing is set to expand on the back of improving real incomes globally, the receding energy crisis, and the need to replenish inventory levels after a long period of de-stocking. This will be supportive to Chinese manufacturing, which is currently suffering from weak global demand, despite the ongoing recovery in the domestic economy.

Second, “bullish” or more optimistic analysts will have to contend with the fact that China’s service recovery is already starting to lose steam and any official support should be limited. Fiscal and monetary stimulus are so far restricted, calibrated to sustain a normal level of activity but not to produce the type of investment booms that were part of the Chinese easing cycles in the past. While additional stimulus are expected between now and 2024, we see no “policy bazooka” this time around. Chinese authorities are keen to see the Chinese economy adjust to a growth model that is less reliant on fixed capital expansion, big infrastructure projects and real estate development. The idea is to favour high-tech manufacturing and consumption. In this transition, long-term growth should naturally moderate.

All in all, Chinese growth has outperformed analyst expectations so far this year, but 2024 remains uncertain. We expect robust but contained 5% GDP growth in China for 2024, as the global manufacturing cycle turns back into expansionary mode and Chinese authorities carefully calibrate their stimulus policies to prevent boom-bust cycles.

Download the PDF version of this weekly commentary in

English

or

عربي