Few topics have been more important for businesses around the world than the economic performance of China. The country has been a major growth leader in recent years, when its economy prompted several bouts of acceleration of the global business cycle. In fact, for every USD 10 of output added to the global economy over the last expansion cycle (2009-2019), China contributed to over USD 4. During this period, China’s growth added to the world an amount equal to USD 10 trillion, which is more than the current GDP of Japan and Germany combined. Moreover, expanding Chinese aggregate demand had a high multiplying effect, spilling over to commodity prices, emerging markets and other open economies.

This time seems to be no different. In 2020, as Covid-19 started its spread in China early in the year, authorities responded quickly with mass testing, virus tracking and effective social distancing measures such as lockdowns and quarantines. As a result, new cases fell down precipitously in the second quarter of the year, allowing the economy to gradually “re-open” before most of the world.

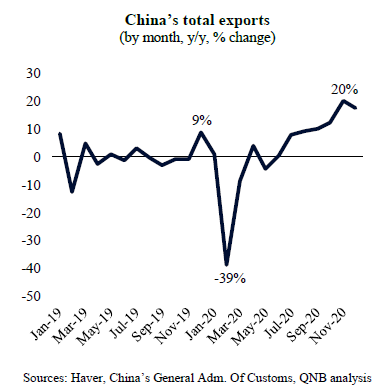

The economic rebound, which started in the second quarter of 2020, after a deep contraction in the first quarter of the year, was also supported by significant policy stimulus in the form of rate cuts, financial support to companies and infrastructure investments. Surprisingly, after an initial sudden collapse of its exports to the rest of the world, the external sector also proved to be supportive for the Chinese recovery. As the world adapted to less face-to-face interactions, more work-from-home and longer periods of social distancing, households adjusted their consumption behaviour, spending less in “experiences” or services and more on physical goods. This produced a boom in Chinese exports, particularly of personal protective equipment, software, electronics and communication equipment. Last month, Chinese exports recorded all-time highs of USD 282 billion, printing high year-on-year growth.

But the strong Chinese economic recovery is now challenged by a wave of new Covid-19 cases around Shijiazhuang, the capital of Hebei province, a northeaster region that is 180 miles from Beijing. After months of near zero new Covid-19 cases, China is now responding to a new cluster of hundreds of cases a day. The response has so far been fast and robust, including the lockdown of over 22 million people and the conduction of mass testing in the region. Lockdowns are expected to be extended to other provinces should new cases emerge, potentially impacting mobility and general economic activity.

In our view, three observations should inform an initial assessment about the impact of such measures in the Chinese economy.

First, a flare up in new Covid-19 cases will have a negative impact on household consumption over the short-term. Chinese families are particularly sensitive to Covid-19 related health risks, which makes individuals more inclined to social distance for longer whenever there is a perception of increased exposure to the virus. Higher frequency mobility data already suggests a decrease in activity beyond the regions directly affected by the new Covid-19 cases, including in higher income provinces of southeast China such as Guangdong. This will weight on consumer-facing service sectors such as accommodation, catering, tourism and offline retailers.

Second, on the supply side, disruption in activity by new social distancing measures should be limited. China’s effective testing and tracking regime will allow for more localized restrictions and for concerted efforts to maintain critical production running. Moreover, Chinese manufacturers are already adapted to Covid-19 preventative measures and potential restrictions are likely to take place during the first quarter, when activity is low due to extended holidays associated with the Chinese New Year.

Third, both existing and potential restrictions are expected to be short-lived. The overall number of new cases is still very low and the Chinese authorities are now experienced in managing the health crisis. This is also supported by high levels of compliance and accountability of the general population to the preventative guidelines.

All in all, despite short-term challenges to household consumption, the Chinese recovery will likely continue. We expect China’s GDP to grow by 8.2% in 2021 and over 6% in 2022, contributing to boost global economic activity.

Download the PDF version of this weekly commentary in English or عربي