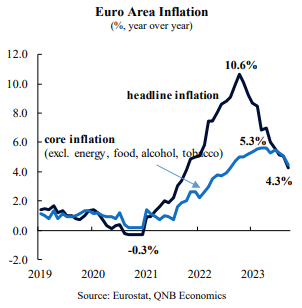

A combination of extraordinary shocks in the Euro Area and the subsequent policy responses resulted in a surge of inflation levels in 2021-2022. During the Covid-pandemic, the lockdowns created supply constraints while loose monetary and fiscal policies boosted demand, producing unusual pricing power for manufacturers and retailers. This turned into an even broader inflationary wave when European economies re-opened, which was later further amplified by the commodity shock trigerred by the Russo-Ukrainian conflict. In fact, headline inflation accelerated rapidly to peak at 10.6% in October 2022 coming from -0.3% in 2020.

The European Central Bank (ECB) responded to the inflationary wave by embarking on a record policy rate tightening cycle, aiming to bring back inflation to its then distant target of 2%. Thereafter, policy rates have been raised 10 times, accumulating increases of 450 basis points to 4.5%. Recently, however, the ECB has been signalling that a halt of the tightening cycle is approaching. According to an ECB statement, interest rates are at levels that if “maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to our target.”

In this article, we discuss why the ECB’s Governing Council is likely to pause the tightening cycle and turn to a “wait and see mode” to assess its impact on the economy.

First, inflation has already fallen considerably from its double-digit peak and continues to consolidate its downward trend. The latest data releases show that headline inflation has more than halved from the 10.6% of October 2022, to 4.3% last month. Core inflation, which excludes the more volatile prices of goods such as food and energy, and is typically more persistent, began to descend in April this year and dropped a substantial 0.6 percentage points (p.p.) in September. Moreover, measures of long-term expectations have been contained, and now stand around the target of 2%. Controlled expectations are crucial to avoid further price pressures from firms and higher wage demands from workers. Overall, falling inflation rates and contained expectations add to the case of a policy rate pause.

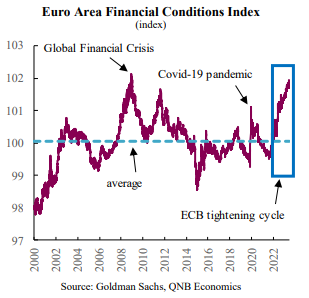

Second, the record cycle of policy rate hikes, combined with the normalisation of the balance sheet of the ECB, have tightened financial conditions to exceptional levels. The Financial Conditions Index for the Euro Area provides a useful summary of the costs of credit. This indicator combines information of short- and long-term interest rates, and credit spreads. The index began a steady upward trend in July 2022 and is currently at a level that has only been registered at the worst of the Global Financial Crisis, when the European economy faced a credit crunch and asset prices collapsed.

In addition to policy rate hikes, the ECB continued to revert the balance sheet expansion that was implemented during the Covid-pandemic to support economic activity. The ongoing “quantitative tightening” will continue to withdraw excess liquidity from the financial system created by extraordinary and temporary measures. Decreased liquidity and higher credit costs have translated into lower volumes of credit, which are now contracting in real terms and will decline further in the coming months.

Third, economic activity has broadly stagnated over the first half of the year and recent indicators point to further weakness in both the service and manufacturing sectors. The Russo-Ukrainian conflict resulted in lower energy availability at higher prices, weighing heavily on the manufacturing sector, with industrial production down 4% from its peak of December 2021. In Germany, the Euro Area’s industrial powerhouse, the energy crisis compounded structural headwinds, such as high taxation and labour shortages, to generate a sharp contraction. German manufacturing is currently 7.4% below the level of February 2020, and continues a downward trend that started in 2017. Across the region, the service sector had supported the economy just enough to avoid a recession in the first semester, but short term indicators show stagnation or even downright contraction during the last several months. With the economy on such weak standing, further tightening could not only be unnecessary, but also risk pushing the economy into a deep recession.

All in all, we expect the ECB to pause the tightening cycle given falling inflation and controlled inflation expectations, severely tight financial conditions, and a weak economy. Going forward, current interest rates will remain in place for a longer period of time for inflation to further converge towards the ECB’s target.

Download the PDF version of this weekly commentary in English or عربي