Gold’s role in the economic and investment landscape has long been a subject of considerable debate. Historically, gold has served as a store of value, safe haven and internationally convertible asset for millennia. In fact, gold has even underpinned the global monetary system during the Gold Standard (1871-1914) and the Bretton Woods System (1945-1971), when major currencies had to be pegged to the yellow metal in order to be considered “convertible” or a true reserve currency.

Despite its non-income-generating nature and the expenses involved in its extraction, gold continues to be held in high regard by investors, including households, sovereign states, and corporations. Its enduring appeal lies in its proven ability to act as a reliable store of wealth, safeguarding assets against periods of significant economic distress and systemic macroeconomic challenges, such as the Great Financial Crisis of 2008-09 or the Covid-19 Pandemic of 2020-22.

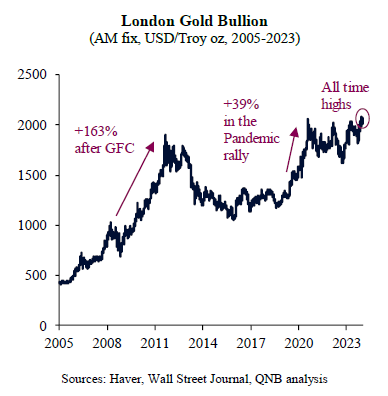

Importantly, after a significant slide from the pandemic highs, gold has recently benefited from a resurgence in demand. As a result, the precious commodity reached an all-time high of USD 2,135 per ounce in December 2023, hovering around those levels ever since. This price strength of gold is ever more surprising in a context where cash or short-dated government securities are offering high nominal yields, which increases the opportunity costs of holding gold. Our analysis delves into three main factors that justify the recent allure of gold for global portfolios.

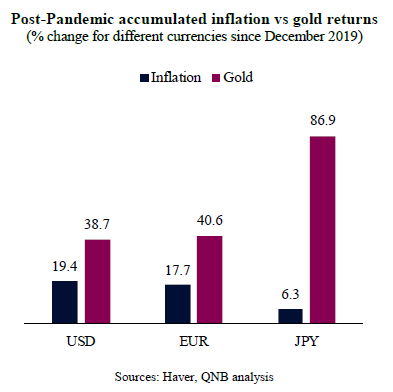

First, gold has recently demonstrated again its enduring value as a safeguard against inflation. In the aftermath of the pandemic, monetary authorities in advanced economies faced significant challenges due to a surge in inflation. This created concerns about the rapid pace of decline in the “real value of money,” as more units of currency would be needed to buy the same baskets of goods and services. Not surprisingly, during this period of higher inflation, gold prices reached all time highs. This offered a compelling affirmation of the long-held belief that gold is an effective hedge against inflationary pressures.

Second, the monetary policy cycle in the US and Europe should soon become a tailwind for gold prices. While nominal yields are now much higher than they were in the recent past in most advanced economies, this dynamic is set to change significantly in short order. The US Federal Reserve and the European Central Bank are expected to cut policy rates by 150 and 100 basis points (bps) this year, respectively. This means that cash and short-dated government securities are going to be less attractive as investment options, favouring alternative investments such as gold.

Third, the current global economic climate is beset with geopolitical uncertainties, such as the Russo-Ukrainian War, ongoing conflicts in the Middle East, and increasing US-China tensions in the Taiwan Strait. These factors can contribute to a heightened risk premium on traditional assets, steering investors to hedge with alternative safe havens. Gold’s appeal has been further bolstered by secular trends, including the intensifying economic rivalry between West and East, a decline in international cooperation, escalating trade disputes, increasing political polarization, and the “weaponization” of economic relations via sanctions. In an era marked by more geopolitical instability, gold’s status as a tangible, jurisdictionally neutral asset that can serve as collateral in various markets becomes increasingly significant. Reflecting this movement, central banks globally have been accumulating gold at a rate unparalleled since the 1960s, when the Bretton Woods System was still operating under the USD-gold peg.

All in all, gold has reaffirmed its position as a cornerstone of alternative investments. Its proven track record as an inflation hedge, coupled with tailwinds coming from monetary easing and the traditional resilience associated with geopolitical upheavals, renders it as an attractive alternative for investors seeking stability and risk mitigation.

Download the PDF version of this weekly commentary in

English

or

عربي