Democratic victories in both special elections in Georgia on the 5th of January have gifted US President-elect Joe Biden control of the Senate - and of Congress overall. The victories are remarkable since Georgia had not elected a Democratic senator since 1996 and President-elect Biden is the first Democrat to win Georgia’s presidential race since 1992.

However, the Democrat majority in the Senate is extremely narrow, depending on Vice President-elect Kamala Harris’s tiebreaking vote, since 50 seats are held by Democrats and 50 by Republicans. Whilst not the “blue wave” that was talked about during the build up to main elections last November, control of Congress will allow the new administration to make more progress with their agenda. Our analysis delves into the implications of Democratic control of both the White House and Congress for the economic outlook via fiscal policy, GDP growth, unemployment inflation, asset purchases and interest rates over the short and medium-term.

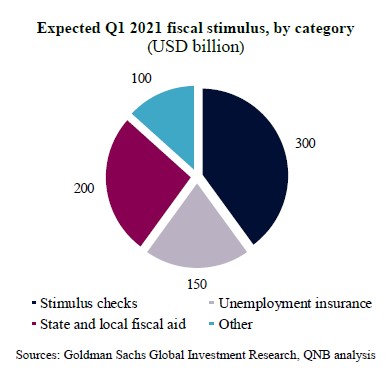

In the short-term, we expect Democrats to now be able to pass legislation that will provide further fiscal stimulus of around USD 750 billion in total during the first quarter of 2021. Goldman Sachs expect this to include USD 300 billion for additional stimulus payments, USD 200 billion for fiscal aid to state and local governments, USD 150 billion to extend both broader eligibility for unemployment benefits and USD 100 billion in other spending (See chart). We expect that the bill to pass towards the end of February with payments beginning soon afterwards.

This new round of fiscal stimulus would further boost disposable personal income as it is in addition to the recently-passed USD 900 billion package, which included USD 600 stimulus checks (for individual adults earning under 75,000 in 2019), additional unemployment benefits and small business support. Fiscal stimulus should add between half and one full percentage point to US GDP growth in 2021. However, the slow pace of vaccination and the emergence of more infectious virus strains will delay and limit the boost to consumer spending.

Moving to the medium-term, we expect the larger amount of fiscal stimulus during the first quarter of the year to be partially off-set by a limited amount of tax increases and spending increases later in the year. Biden’s fiscal policy agenda is expected to substantially increase the expenditure side, particularly social investments associated with entitlements, education and healthcare, although likely in much smaller amounts than originally proposed by the Biden campaign during the build-up to the November election. Funding is set to be provided by additional taxation, as Biden proposes to raise taxes and reduce benefits of upper-income taxpayers.

Stronger GDP growth is expected to reduce unemployment and we now expect the unemployment rate to fall below 5% by the end of 2021. This reduced slack in the labour market should lead to slightly firmer inflation, with policy changes to healthcare prices giving an additional boost to inflation in 2021. Lower unemployment and higher inflation mean that the Fed will taper asset purchases (i.e. begin to reduce asset purchases) and raise interest rates earlier than previously expected. However, we do not expect tapering to begin before the end of the year and the so-called “liftoff” (i.e. when the Fed begins to raise interest rates) is unlikely for a number of years because average inflation targeting gives the Fed plenty of policy space to keep interest rates low for a considerable period of time.

Outside of fiscal policy, most other legislation will require support of at least 60 Senators to pass because of opposition to eliminating the filibuster. This means that bipartisan support will still be required to pass legislation on topics such as infrastructure, a minimum wage increase, tech regulation, and environmental policies. However, Democratic control of the Senate will still make a difference in those areas, as Democrats will now control the agenda in the Senate, and Biden will have more freedom to nominate officials to influential policy positions that a Republican Senate majority would have been able to block. We also see some scope for bipartisan cooperation on an infrastructure package.

Democratic control of Washington, DC after Inauguration day on the 20th of January will bring greater fiscal spending, faster GDP growth, more inflation and higher interest rates than we had previously assumed. In any case, the US is set to continue being an economic powerhouse that spurs technology and innovation across the globe.

Download the PDF version of this weekly commentary in English or عربي