Early this month, the central bank finally decided to pivot its monetary stance, cutting policy rates by 25 basis points (bps). The decision was expected, coming two years after the start of a record tightening cycle of 10 consecutive rate hikes that took the benchmark Euro area deposit rate to 4%.

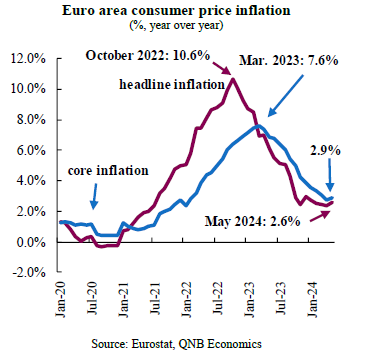

Importantly, the move was also historic, as this is the first time ever in which the European Central Bank (ECB) started an easing cycle ahead of the usually more “dovish” US Federal Reserve (Fed). Moreover, the decision took place amid concerns that above target (2%) inflation is re-accelerating, after months of significant moderation. In fact, headline inflation was running at 2.6% in May, while core inflation, which extracts the more volatile elements of energy and food prices from the reference basket, was at 2.9% for the same period.

In our view, despite still lingering inflation concerns, this decision marks the beginning of a gradual cycle of interest rate cuts. In this article, we discuss the three main factors that support our outlook.

First, inflation is consolidating its steady convergence towards the ECB’s target, which supports additional interest rate cuts. Inflation is now slightly more than than half a percentage point away from the monetary policy objective. An important measure for policy is core inflation. By excluding the more volatile components, core inflation provides a more stable and informative view of the underlying inflation trends. The peak in core inflation was reached at 7.6% in March last year, after which it started a steady downward trend, reaching 2.9% in the most recent release. The disinflation cycle is expected to continue, irrespectively of volatility and negative data surprises.

Moreover, measures of long-term expectations have stabilized at the target of 2% for two consecutive quarters. Controlled expectations are crucial to moderate further price pressures from firms, as well as higher wage demands from workers. Overall, with inflation close to reaching the ECB target, and contained inflation expectations, the case was built for the beginning of a policy rate reduction cycle.

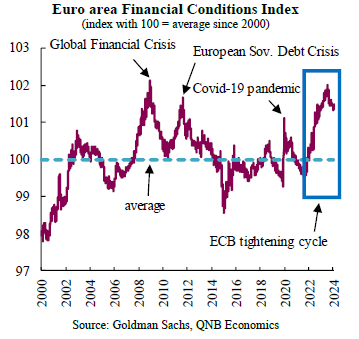

Second, the record cycle of policy rate tightening, together with the normalisation of the central bank’s balance sheet, have left financial conditions at exceptionally restricted levels. The Financial Conditions Index for the Euro area provides a useful summary of the costs of credit. This indicator combines information of short- and long-term interest rates, and credit spreads. The index spiked in mid- 2022 and is currently at levels that have only been reached at the worst of the Global Financial Crisis, when the European economy faced a credit crunch and asset prices collapsed, or during the European Sovereign Debt Crisis.

In addition to policy rate hikes, the ECB continued to revert the balance sheet expansion that was implemented during the Covid-pandemic to support economic activity. The ongoing “quantitative tightening” will continue to withdraw liquidity from the financial system created by extraordinary and temporary measures. Decreased liquidity and higher credit costs have an impact on the volumes of credit, which are contracting in real terms, and are likely to decline further in the coming months, an indication to the ECB that its tightening cycle has been effective.

Third, the Euro area has just experienced a mild recession in H2-2023, and its economic growth performance is expected to remain lackluster. The most recent prints of the Purchasing Managers Index (PMI) signal a stagnant economic outlook. The PMI is a survey-based indicator that provides a measurement of improvement or deterioration in economic activity. This year, the composite PMI, which tracks the joint evolution of the services and manufacturing sectors, has remained below or close to the 50-point threshold that separates contraction and expansion. In line with this indicator, the Bloomberg consensus points to a modest growth in real GDP of 0.6% this year. While we do believe that there is scope for positive surprises in Euro area activity this year, our less negative 0.9% growth projection is still much below the long-term growth of 1.5%. Hence, growth is expected to remain well below trend, and therefore require some support from policy easing.

All in all, the cut of policy rates by the ECB was supported by the still ongoing disinflation cycle, and overly-restrictive financial conditions in an environment of below trend growth. We expect the easing cycle to be gradual, absent significant unexpected developments in inflation, with two additional 25 bps cuts this year, as the ECB continues to monitor the evolution of prices and economic activity.

Download the PDF version of this weekly commentary in English or عربي