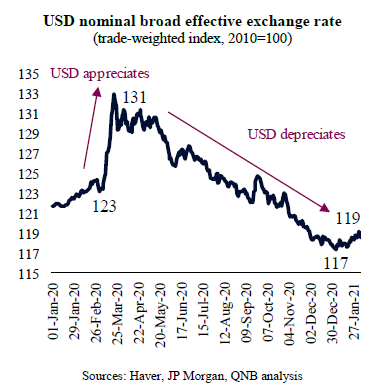

Early last year, as the Covid-19 pandemic started to plague the global economy with a flash crash in activity, investors were shocked into one of the fastest sell-offs of risk assets ever recorded. In the process, the overall run for liquid, safe-haven assets made investors pile into the US Dollar (USD). In fact, the USD appreciated by more than 8% against a basket of trade-weighted currencies in February and March 2020.

But the USD bull run did not last long. As the US had more monetary policy room than the other advanced economies, aggressive interest rate cuts by the Federal Reserve narrowed the interest rate differentials versus the rest of the world, favouring capital flows to non-USD assets. This led to a depreciation of the USD. After half a year of a steady downtrend, the USD broke below pre-pandemic levels on a trade-weighted basis in November.

More recently, despite vaccine optimism and upward revisions of global growth prospects, the USD has steadied across the board. This happened on the back of renewed Covid-19 fears (with new cases soaring) and a slowdown in the recovery process outside the US, particularly in Europe. This led investors to question whether such foreign exchange (FX) movements are just a short pause on a longer downtrend phase for the USD or if a reversal of FX trends is imminent.

In our view, the current consolidation of the USD is likely an intermediate-term movement (3 to 6 months) predicated in three main pro-USD drivers.

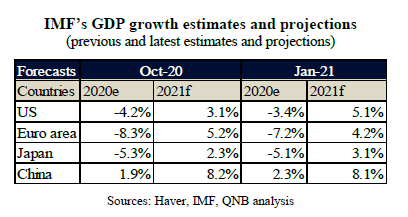

First, growth expectations and momentum suggest that the US will outperform other major economies, which should boost the USD. The IMF has just upgraded their growth projections for the US in 2020-21 by 290 basis points (bps), against 100 bps for Japan, 30 bps for China and only 10 bps for Europe. The US is favoured by a more rapid deployment of Covid-19 vaccines and bigger as well as more stable policy stimulus. Capital flows tend to follow growth expectations, with investors bidding for the currencies of countries with positive economic performance.

Second, a stronger recovery with higher inflation expectations in the US has so far driven long dated US Treasury (UST) yields up, widening the spread between UST and European or Japanese bonds. This movement is set to persist as US economic outperformance continues and central banks in Europe and Japan maintain their policies of stricter controls for long dated yields (sustaining ultra-low or negative interest rates). Expectations for higher yields in the US are likely to lead to capital flows into US assets, supporting the USD.

Third, speculative positioning against the USD in FX future markets reached multi-year records in late January, an extreme that normally suggests a currency is oversold and set for a reversal. Hence, a rebalancing of FX positioning will likely create additional demand for the USD.

All in all, the USD is in the process of consolidating further, potentially re-gaining some ground lost during its depreciation in 2020. Tailwinds for the USD over the coming months include favourable growth expectations, positive interest rate differentials and extreme short positioning.

Download the PDF version of this weekly commentary in English or عربي