Few indicators convey as much information about the state of a country’s economy as the direction of currency fluctuations. This is particularly valid when it comes to deep, liquid foreign exchange (FX) markets of major currencies from advanced economies, such as the Japanese Yen (JPY), the US Dollar (USD), the Euro (EUR), the Swiss Franc (CHF) and the Pound Sterling (GBP). FX is driven by capital flows, which correspond to real time reactions to expectations about risk appetite, relative economic performance and interest rate differentials.

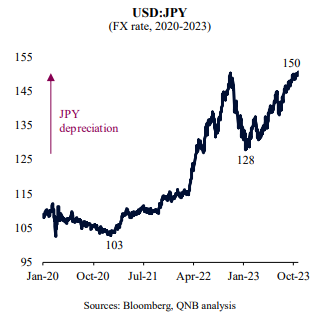

In recent months, the Bank of Japan’s (BoJ) ultra-loose stance amid a period of aggressive tightening by the US Federal Reserve (Fed) and European Central Bank (ECB) favoured capital outflows from Japan. This affected the JPY, which depreciated further back towards multi-decade lows, down by 46% from post-pandemic highs.

The JPY move did not happen in a straight line. At the beginning of the pandemic, the JPY was supported by significant “global recessionary, safe-haven” demand. This is because the JPY tends to be inversely correlated to the global business cycle, given that lower commodity prices tend to favour the JPY and local investors are heavily exposed to overseas assets but often “repatriate” large volumes of capital during periods of financial stress. However, shortly after the negative pandemic shock, the JPY started to depreciate. The movement gained further momentum in Q2 2022, after other major central banks initiated their monetary tightening cycle. The JPY then recovered temporarily in late 2022 and early 2023, as it was expected that the Fed would reverse its tightening stance which would narrow the interest rate differential with Japan and strengthen the JPY. As global growth proved resilient and central banks leaned “hawkish,” the JPY depreciation resumed. This leads to the question: is the JPY sell-off overdone? What can we expect moving forward?

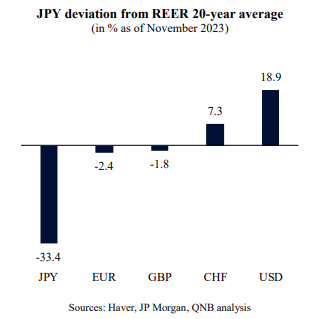

A common way to look at currency “valuations” is to analyse trade-weighted, inflation-adjusted exchange rates, i.e., the real effective exchange rates (REER), and compare it to their own long-term averages or historical norms. This REER metric is more robust than traditional FX rates as it captures changes in trade patterns between countries as well as economic imbalances in the form of inflation and inflation differentials.

The REER picture for November 2023 suggests that the JPY is indeed by far the most undervalued currency in the advanced world, by more than 30% of its notional “fair value.” In our view, however, conditions are expected to favour a recovery of the JPY over the medium-term. This is predicated in our expectation that interest rate differentials should move significantly in JPY’s favour over the next several quarters.

The BoJ is on the verge of gradually tightening its monetary policy stance. This would mark an exit to a long period of ultra-loose policies that kept short-dated rates negative and 10-year yields on government bonds capped at only 0.5%. At its July policy meeting, the BoJ lifted the upper bound of its target range for the 10-year yield to 1%, starting the long-awaited process of dismantling the yield curve control (YCC) framework. We expect a further tightening next year, with a full exit from YCC (no caps for 10-year yields) in Q1 and an initial hike of the short-term policy rate in Q2.

These moves are likely to take place on the back of a higher level of confidence from BoJ’s officials that the country is finally breaking away from its “deflationary trap.” Inflation has been consistently above target this year and wage growth has so far proved to be both significant and persistent.

In contrast, policy rates are set to “peak” across most other advanced economies over the coming months, leading to stable rates for longer. In other words, there is little scope for much higher rates outside Japan. Moreover, if the global economy slows down and some key economies enter a recession, rates could be cut significantly in the US and Europe. In any scenario, the interest rate differential between the JPY and other major currencies would narrow in favour of the JPY, supporting the undervalued currency.

All in all, we expect to see at least a partial reversal of the ongoing JPY weakness over the medium-term. The currency’s undervaluation, coupled with the likely direction of policy rate differentials, should favour a significant JPY rally.

Download the PDF version of this weekly commentary in English or عربي