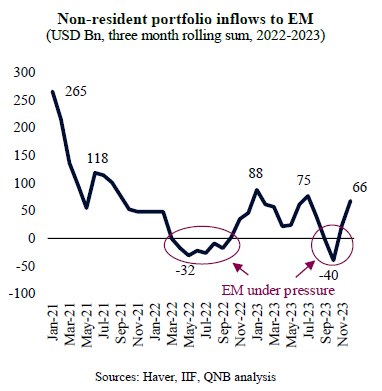

Over the last two years, emerging markets (EM) suffered from significant volatility in capital flows. This was driven by monetary instability, geopolitical uncertainty and a lack of broader risk appetite from global investors.

According to the Institute of International Finance (IIF), non-resident portfolio inflows to EM, which represent investments from foreign investors into local public assets (listed equities and bonds), turned negative twice in recent years. This happened both during March-September 2022 and August-October 2023, when pressure was at the highest.

At these times of pressure, EM headwinds included a strong USD, high and rising interest rates in major advanced economies, and a deep global manufacturing recession. As a result, outflows led to a challenging environment for EM assets, which continued to underperform benchmark returns from advanced economies.

In fact, the MSCI EM Index, which captures large- and mid-cap EM-based equities from 24 key jurisdictions, including some of the most dynamic economies of Asia, Latin America, the Middle East and Africa, declined by about 26% since early 2021. In contrast, the S&P 500 Index of leading businesses listed in the US gained almost 30% over the same period.

In our view, however, this underperformance is set to moderate or partially revert, as risk appetite returns and capital flows to EM resume. Two main factors sustain our opinion of an increasingly more benign global macro backdrop for EM: a shift in relative macroeconomic performance and the gradual adjustment of interest rate differentials between US and major EM.

First, the US growth relative “exceptionalism” is expected to moderate. Over the last couple of years, a flurry of negative economic data surprises in most major EM versus positive surprises in the US led to several rounds of revisions in relative growth expectations in favour of the US. This pulled global capital into the US, further drying up liquidity elsewhere. But this dynamic is already starting to change.

The wide gap in favour of the US in the Citi Economic Surprise Index had already narrowed significantly since late 2023, suggesting that the period of growth revisions favouring the US will come to an end. Moreover, the growth differential between the US and EM, which was very narrow at 180 basis points (bps) last year, should revert to a more standard 250 bps this year. Hence, the growth gap is expected to re-widen in favour of EM, pushing capital back to this dynamic jurisdictions.

Second, interest rate differentials are set to also favour EM assets and non-USD currencies against US assets and the USD. After many months being overheated, the US economy is finally slowing down. This, alongside a normalization of supply chains from the pandemic and geopolitical disruptions, is already supporting a rapid return of monetary stability. Inflation rates are set to quickly converge towards the 2% central bank target.

Such macro backdrop is favouring a “dovish” pivot from the US Federal Reserve, with aggressive policy rate cuts expected throughout the year. Markets are currently pricing Fed fund rates to end the year at 3.75%, or 175 bps below the existing rates. This should boost global liquidity and push capital overseas in search for higher yields and returns globally, particularly in EM.

All in all, after a period marked by volatile capital flows and market underperformance, a more benign environment for EM should emerge. Both relative growth and interest rates should present a more favourable proposition to EM, with both non-resident capital flows and asset returns normalizing.

Download the PDF version of this weekly commentary in

English

or

عربي