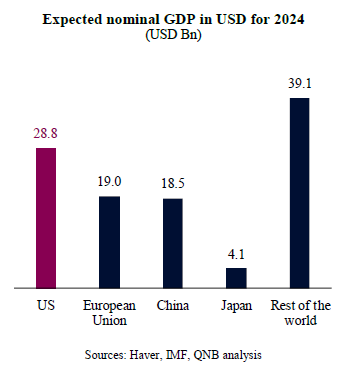

It is often said that the US election is not purely an American concern, as the country’s power, wealth and influence reverberate globally. In fact, with a nominal GDP of USD 28.8 trillion (Tn), far outpacing any other major economy, and a household net worth of more than USD 150 Tn, the US is at the core of global movements of information, capital, goods and services. No other country plays a similar role in determining the direction of the global economy.

Hence, it is important to understand the implications of the US election for the global economy, particularly as each of the two main candidates (Donald J. Trump and Kamala Harris) withhold different economic agendas.

This week, we dive into the economic programme of candidate Trump, former president who is trying to return to the White House and become the 47th president of the US.

After serving as the 45th president of the US in 2017-2021, Trump’s agenda is well known for investors and analysts: the slogans “Make America Great Again” (MAGA) and “America First” summarize the general ethos of his platform. In practical economic terms, this translates into a pro-business, pro-capital, mercantilist, pro-domestic manufacturing policy. In other words, Trump supports de-regulation and less red tape in key industries, lower taxes for corporates and households, more public investments and subsidies for domestic manufacturing and defence, and a protectionist stance on foreign trade.

Some of the measures supported by Trump are materially different from the policies being currently implemented. In our view, three main points should be highlighted regarding Trump’s economic agenda.

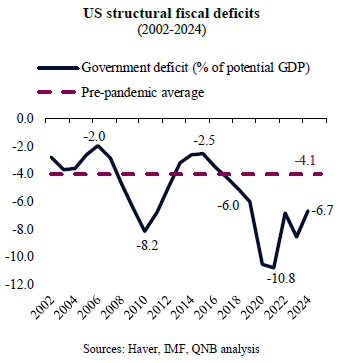

First, if elected, Trump tends to be aggressive in terms of fiscal stimulus. In fact, during his term as president, tax cuts and higher spending took government deficits from a lower than average 3.6% of potential GDP to 6% in 2019, before the pandemic required even wider deficits. Currently, Trump is proposing a reduction in corporate taxes from 21% to 15%. Importantly, the individual tax cuts that he approved in 2017, which are set to expire at the end of 2025, are likely to be extended under his potential presidency. Taken together, those fiscal measures are expected to cost USD 3 trillion (Tn) to USD 4 Tn in revenues, further widening the already critical deficit. But this should provide a boost to the economy, supporting both investments and consumption. This should also support long-term US Treasury yields and a normalization of the yield curve, as wider deficits and higher levels of debt-to-GDP could scare some fixed-income investors and require higher term premiums.

Second, Trump seems to be committed to re-launching his protectionist agenda. He is defending the imposition of higher external tariffs of 10% minimum on the rest of the world and 60% on China in particular. If such measures were to be fully implemented under a potential Trump administration, and not only used as leverage for trade and investment negotiations, they would likely create a significant shock for trade and investment flows. Other countries would likely retaliate, potentially creating a spiral of “beggar-thy-neighbour” competitive currency devaluations and tariff hikes. Importantly, higher tariffs would not generate enough revenues to cover for tax cuts. Higher tariffs are estimated to generate about USD 1.5 Tn in additional revenues, less than half the estimated cost of the proposed tax cuts. In terms of high-level impacts, higher tariffs would be negative for aggregate global and US real incomes, due to higher costs of final goods and services. But it would potentially benefit investments and domestic manufacturing, as supply chains would need to be re-allocated and new arbitrage conditions would be formed in favour of local producers.

Third, Trump’s stance on immigration may also have significant implications for the country’s demographics and labour markets, should the former president return to the White House. Trump suggested not only the mass deportation of 15 to 20 million undocumented migrants, but also restricting the inflow of visa-holding legal migrants. This is significant, even for a country with a population of more than 335 million people and a labour force of 162 million. While we do not expect this to be enacted at this scale if he is elected, even a less aggressive deportation programme would contribute to tighten labour conditions, particularly in the low-wage hourly compensation space. Over the medium term, this could increase the average wage growth, creating additional inflation pressures. A less positive demographic profile would also be negative for growth.

All in all, an eventual Trump presidency “2.0” would bring significant change to the US economic agenda, particularly on the fiscal, trade and migration spaces. Taken together, the proposed agenda should be a mixed bag for growth, as fiscal policies would boost activity, whereas trade protectionism and a stricter handling of migration would weigh on GDP expansion.

Download the PDF version of this weekly commentary in

English

or

عربي