Before the Covid-pandemic, Southeast Asia was one of the most dynamic regions in the world with the highest growth outlook. The six largest economies of the Association of Southeast Asian Nations (ASEAN-6), which includes Indonesia, Thailand, Singapore, Malaysia, Vietnam, and the Philippines, have been some of the fastest growing economies in recent decades. With the end of the Covid-pandemic and the reopening of China, it was expected that these countries would return to the strong growth rates of previous years. But 2023 turned out to provide a less supportive environment than had initially been projected, and expectations have adjusted accordingly.

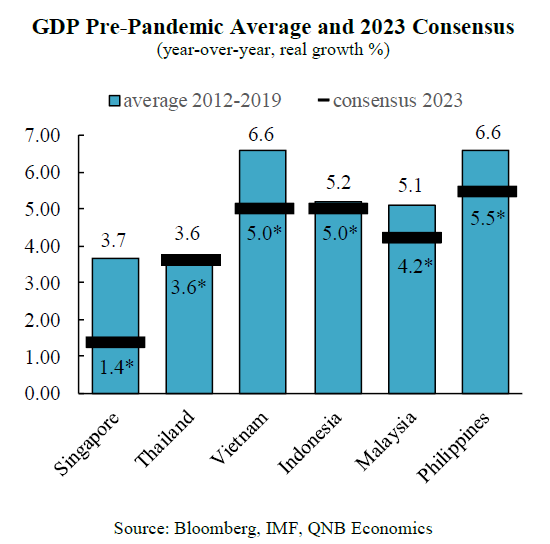

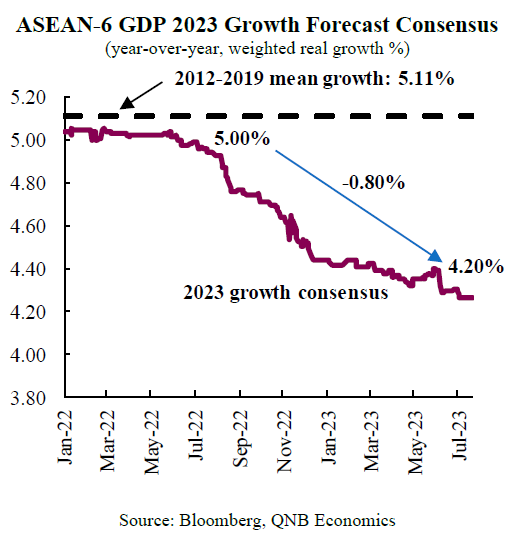

The Bloomberg consensus is a useful tool to track economic forecasts from economists, think tanks, and research houses. It allows to compare growth expectations with historical performance, as well as to track them over time. The forecasts show that growth this year will be weaker across the different ASEAN-6 economies than their pre-Covid pandemic averages of 2012-2019. Additionally, the overall 2023 growth forecast for ASEAN-6 has fallen since mid-2022 by 0.80 percentage points (p.p.), from 5% to 4.2%, below the average of 5.1% for the region during 2012-2019. In this article, we discuss three main factors behind the performance of the ASEAN-6 this year.

First, higher interest rates and tighter financial conditions in the major advanced economies, as well as in the ASEAN-6 countries, currently imply a less favourable environment for growth. In advanced economies, financial conditions are at the tightest levels in years. The US Federal Reserve and the European Central Bank have increased their policy interest rates by 525 and 400 basis points (bps), respectively, since the first half of 2022. Although it is still unclear when these cycles will be complete, higher interest rates are expected to remain in place for longer in the major advanced economies.

Central banks in ASEAN-6 have implemented their own monetary tightening cycles in order to contain domestic inflation. In these economies, the average increase in policy rates was 230 bps, with the most aggressive sequences carried out in the Philippines and Singapore, with accumulated increases of 425 and 400 bps, respectively. Even as some of the central banks in this region are expected to reach a turning poing in their monetary policy, domestic and international tightening already had an impact on growth this year, and high interest rates will continue to be a drag on activity going forward.

Second, weak external demand translated into a slowdown in the growth of international trade, which is particularly relevant for the globally integrated ASEAN-6 economies. Trade volumes fluctuate in sync with the global cycles of economic expansions and contractions. As the global economy decelerated so far this year, the impulse for international trade weakened. Growth in international trade volumes is expected to be approximately 1.7% in 2023, a weak mark compared to the 2.5% of the 5-year pre-Covid pandemic period of 2015-2019, adding another factor that contributes to lower economic growth in the ASEAN-6 economies.

Third, after the large expansionary fiscal policies that were implemented to support the economies during the Covid-pandemic, governments now face the need to normalize their debt and spending levels. Between 2019 and 2021 the level of government debt relative to GDP, increased by more than 10 p.p. in the ASEAN-6 economies. The increments were as high as 20 p.p. in Philippines and Singapore, and 17 p.p. in Thailand (the single exception was Vietnam, were the ratio actually fell by 1.5 p.p.). Now, with increasing interest rates and the pressing need to rebuild fiscal buffers, governments are on their way to stabilise their fiscal policies and control their levels of debt.

According to the International Monetary Fund’s estimates, ASEAN-6 countries are overall reducing their fiscal impulse this year. For example, government expenditures in Malaysia are expected to be reduced by 7% this year in real terms. The exception is Vietnam, where strong GDP growth would allow the country to reduce the ratio of debt of GDP even as it increases real spending. Thus, with the exception of Vietnam, fiscal policy in the ASEAN-6 countries is less supportive for growth, and will therefore contribute to a weaker performance in 2023.

All in all, growth expectations for the ASEAN-6 economies have been adjusted for this year, on the back of tighter domestic and international financial conditions, weaker external demand, and less supportive fiscal policies. While growth is still robust by international standards, it is below its pre-pandemic historical performance.

Download the PDF version of this weekly commentary in

English

or

عربي