The US Federal Reserve (Fed) is expected to keep its benchmark policy rate unchanged at its March and May 2024 Federal Open Market Committee meetings. These decisions should extend the “pause” of the tightening cycle that started a year ago, after eleven rate hikes pushed the Fed funds policy rate to the highest levels in more than two decades at 5.25-5.5%.

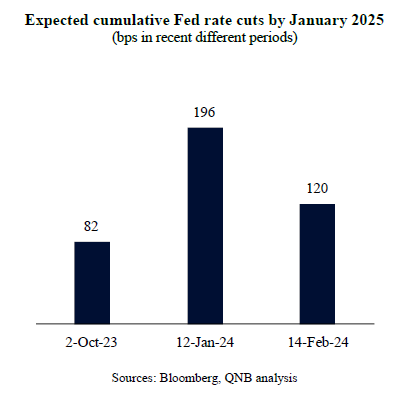

Late last year, amid a sequence of positive surprises with lower than expected inflation prints, fixed income markets started to suggest an aggressive schedule of rate cuts by the Fed for 2024. Fed officials even set the stage for the beginning of an easing cycle with “dovish” remarks by the end of last year. This triggered a wave of optimism in both equity and bond markets, as lower expected cash rates favoured a return of allocations to riskier investments. In fact, at peak optimism, markets were pricing almost 200 basis point (bps) policy rate cuts throughout the year.

However, as the most recent inflation prints for January 2024 came in higher than expected, investors’ confidence in an aggressive dovish pivot by the Fed towards deep rate cuts started to be partially reversed.

This re-started the debate about whether the Fed is ready to go through with rate cuts, keep the rate pause for longer or even abandon the dovish pivot altogether. In our view, under current conditions, the Fed is likely to follow through with the dovish pivot, cutting rates significantly over the next few quarters. Three main factors support our analysis.

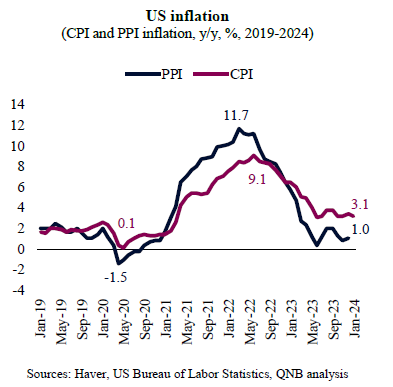

First, inflation has moderated significantly and is expected to moderate further in the coming months. Consumer price inflation (CPI) has peaked in September 2022 and slowed down to close to 3% in recent months, however still away from the 2% Fed target. Importantly, the producer price inflation (PPI), which has been leading headline inflation by around a quarter, has decreased rapidly. This is due to a normalization of supply chains as the effects of the re-opening of the economy have stabilized. This, alongside other leading indicators, such as global input prices, suggest that inflation will fall further towards the Fed target over the coming months, opening the door for more rate cuts this year.

Second, US consumption is set to moderate on the back of a less benign environment for real incomes and the headwinds from the 2022-23 monetary tightening. US consumers are unlikely to benefit from the same type of tailwinds that supported disposable incomes in 2023, given that the inflationary pressures already subsided and interest rates are still elevated. The sharp correction in commodity prices favoured a significant boost in disposable incomes, especially as wage growth was robust, supporting consumption. Going forward, there is limited room for commodity prices to decline further and labour markets already eased, pointing to lower wage growth. In addition, as monetary policy operates with long and variable lags, the effects of the previous rate hikes from the Fed will start to weigh on consumers, especially as more homeowners are affected by costlier mortgages.

Third, the political agenda may also prevent the Fed from taking bold action or surprising the markets too much. This is because significant shocks to expectations may have an impact on the 2024 US presidential election, benefitting the incumbent or the opposition. Traditionally, the Fed tends to take the charted path during major election years, avoiding dramatic moves or taking actions that would upset stakeholders and raise questions about political leanings. In this case, the charted path would be following through with the dovish pivot, delivering rate cuts in Q2 and Q3 2024.

All in all, we expect the Fed to cut rates by 100-125 bps throughout the year, starting in June. This is predicated on the significant and expected moderation of inflation, the incoming slowdown of household consumption and the US presidential election, which should limit the degree of freedom of the Fed in 2024.

Download the PDF version of this weekly commentary in

English

or

عربي