Every summer, the European Central Bank (ECB) organizes a coveted monetary policy forum in Sintra, Portugal. The event is one of the most important central banking conferences in the world, bringing together top economists, bankers, market participants, academics and policy makers to discuss long-term macro issues.

Since its inception in 2015, the forum has garnered significant attention due to the impactful speeches delivered by senior policymakers, rivalling the Jackson Hole conference in its appeal to investors.

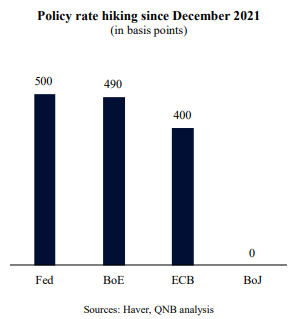

As an ECB-led event, it has always held prominence on investors’ calendars. However, this year’s meeting was of unparalleled importance, featuring attendees, such as governors from major central banks like the ECB, the US Federal Reserve (Fed), the Bank of England (BoE), and the Bank of Japan (BoJ). Moreover, it followed a period where major central banks had to catch up with above target inflation that led to aggressive mulit-decade high policy rate hiking.

As the effects of tighter monetary conditions start to weigh on economic activity, there is now significant uncertainty about what comes next: are major central banks done with the hiking cycle? Should we expect a long monetary policy “pause”? Are rate cuts in the pipeline for later this year?

In our view, insights shared during the meeting by senior central bank officials point to three major conclusions: policy rates are likely to see further hikes, the slowdown in growth will continue, and Japan continues to be the big exception when it comes to monetary policy.

First, despite expectations at the beginning of the year about an early “dovish” pivot from major central banks to rate cutting, policy tightening is still the order of the day for the Fed, ECB and BoE. Advanced economies have proven to be more resilient than previously expected and this is justifying a steady course from monetary authorities. The Fed’s chairman, Jerome Powell, reinforced that irrespectively of the latest “pause” in interest rate hikes; more hikes are likely to be appropriate. Similarly, Christine Lagarde, president of the ECB, pointed that there is still “ground to cover” on the interest rate front. The governor of the BoE, Andrew Bailey, maintained a “hawkish” stance.

Second, monetary policy authorities conceded that an sharper economic slowdown is inevitable and reiterated that a shallow recession or a moderate weakness will not change their path. Although, all senior officials refrained from directly addressing their readiness to withstand recessions, governor Bailey underlined the BoE’s previous recession forecasts, coupled with their unrelenting stance on tightening policy. Moreover, chair Powell and president Lagarde admitted the plausible occurrence of recessions over the next few quarters, subtly suggesting their acceptance of such scenarios as a necessary sacrifice to curb persistent high inflation.

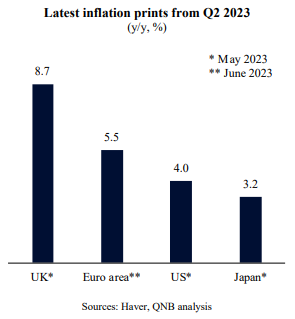

Third, the BoJ holds a very different stance from other major central banks. The BoJ’s governor, Kazuo Ueda, pointed out that despite an increase in core inflation, essential price pressure indicators like wage growth are still insufficiently aligned with the BoJ’s objective for long-term inflation in Japan. He predicted an impeding short-term dip in inflation, followed by a surge next year. Only with unequivocal evidence of the latter would he feel at ease moderating any policy accommodation.

All in all, with the noteworthy exception of Japan, senior officials from major advanced central banks decided to convey a “hawkish” tone at the Sintra forum. After a late start to tightening cycles last year, which further enabled significant overshoots in inflation, central banks remain on a mission to regain credibility. This is likely to make them lean “hawkish” amid uncertainty.

Download the PDF version of this weekly commentary in

English

or

عربي