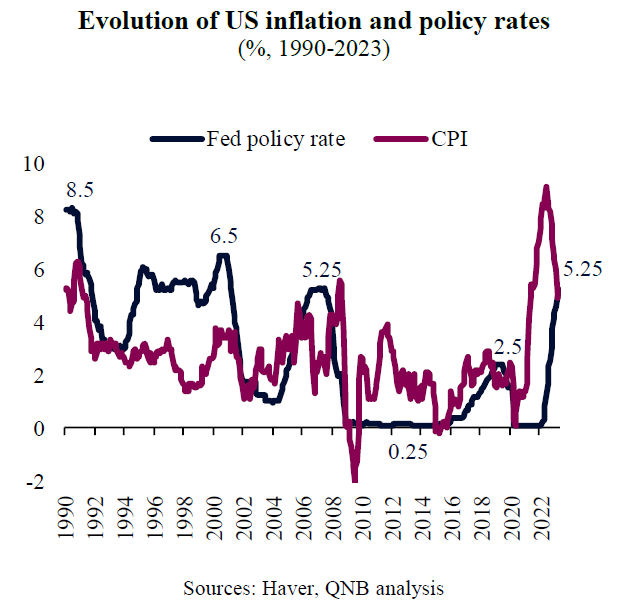

The US Federal Reserve (Fed) has kept its benchmark policy rate unchanged. This finally halted the cycle that reverted a decades-long approach of ultra-easy monetary policy. The decision took place after ten rate hikes since March last year, when untamed inflation forced the Fed to increase policy rates for the first time in more than three years.

Altogether, the 500 basis points (bps) increase in interest rates so far is shaping one of the most significant and unexpected monetary tightening cycles in US history. From a long period of record low interest rates, policy rates are now at the highest in a generation, equalling the top range of all hiking cycles since the early 2000s.

The latest decision marks a pause of the tightening cycle, bringing the current Fed funds rate to a level of 5.00-5.25%. In our view, three main factors stand behind this decision, as we keep in mind that the Fed’s formal monetary policy framework targets an average 2% inflation rate.

First, short-term policy rates have already “normalized.” After several months having to catch up with surging consumer prices, Fed fund rates have now consolidated above the current inflation rate. Reasons behind this normalization include both the recent aggressive policy stance from the Fed and a significant moderation in inflation. Importantly, inflation has been trending down for ten straight months and is expected to moderate further, projected to run close to 3% by December this year.

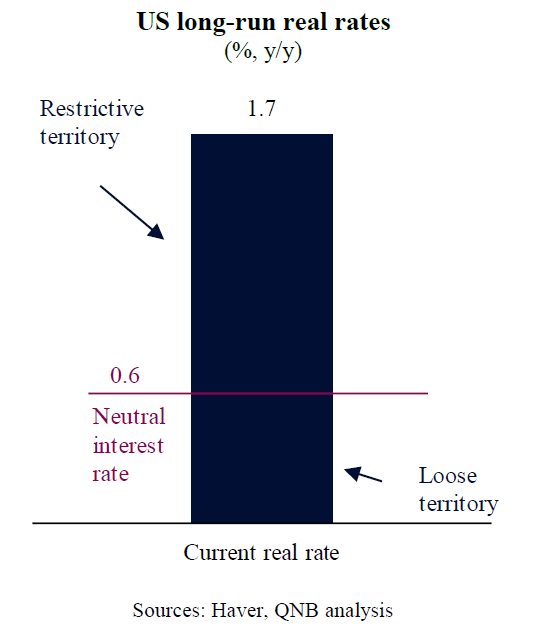

Second, current long-term real rates, which subtract inflation expectations from nominal yield, are in restrictive territory, as indicated in the above graph. In fact, the current real rate of 1.7% is significantly above the Fed estimates for neutral real interest rates. This means that rates are set to act as a drag in activity and employment, supporting a further moderation of inflation. In addition, it is unclear when the effects of the recent hikes by the Fed will slow down the economy. Therefore, it is understandable that the Fed would prefer to wait and see how the economy reacts to higher interest rates before taking the risk of pushing monetary conditions further into restrictive territory.

Third, US regional banks with large unrealized losses on their Treasury bond portfolios witnessed large deposit outflows, creating financial instability. This lack of confidence led to rapid bank runs on more vulnerable entities, such as California-based Silicon Valley Bank and New York-based Signature Bank. Fears of contagion then emerged, creating liquidity pressures across the entire spectrum of domestic regional banks. As a result, banks are tightening their lending standards in an effort to reduce credit commitments. This creates a bank induced tightening of financial conditions beyond any additional Fed action, taking pressure off from the Fed when it comes to more policy hikes.

Despite the decision to pause interest rate hikes at current levels, we do not expect to see a “pivot” or policy rate cuts anytime soon. We are rather expecting a long “pause” until new data presents a clearer path for policymaking. Labour markets are still too tight, favouring wage growth rates that are inconsistent with below target inflation.

All in all, the case for a Fed “pause” is supported by normalized policy rates, restrictive real rates, and financial instability. We therefore expect rates to remain at their current 5.00-5.25% levels until at least Q2 2024. A gradual moderation of labour markets requires a restrictive monetary policy stance for longer, preventing an early turn to a more “dovish” stance with lower rates.

Download the PDF version of this weekly commentary in

English

or

عربي