International trade allows nations to access goods and services that otherwise may not have been available. As a result, international trade creates comparative advantages resulting in higher productivity, efficiency gains, better pricing and overall economic growth. Global trade activity is a traditional indicator for the health and direction of the overall economy. Expanding flows of goods and services tend to be associated with productivity gains and prosperity.

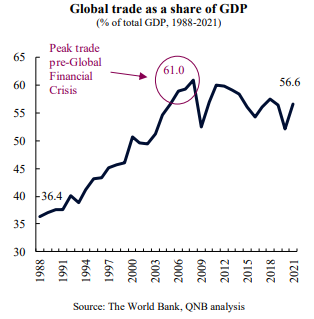

Global trade peaked just before the Global Financial Crisis. However, the recent geopolitical tensions between the US and China and its spill-over effects to other regions and countries are generating global economic uncertainties. This is negatively affecting trade, supply chains, and investment flows. New border frictions through tariffs and non-tariff barriers, additional regulation and administrative costs, and economic policy volatility are some of the obstacles faced by firms in this new economic landscape.

This piece dives into a case study of how “economic disintegration” can lead to economic underperformance: the post-Brexit UK. Certainly, multiple other major events and shocks have disrupted the global economy in recent years. Nevertheless, increasing evidence is showing that the process that began with the UK’s vote to leave the European Union can be attributed an important role.

The official monthly estimate of GDP shows that economic activity in the UK has grown by just 0.3% since the beginning of 2022, and is still below its pre-pandemic levels by 0.4%. In contrast, in the 5 year period of 2011-2015, which precedes the Brexit referendum of 2016, annual growth was significantly higher, averaging 2.2%. The UK is also lagging behind the major continental European economies. The UK’s “Euro Peers,” defined as the group of the three largest economies of the European Union (Germany, France, and Italy), have already outpaced their pre-pandemic GDP by 1.2%.

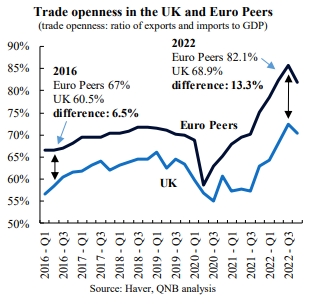

In mid-2016, at the moment of the referendum, trade openness in the UK was 60.5% of GDP. This was 6.5 percentage points (p.p.) lower than the average value of 67% for the Euro Peers. In 2022, this difference had increased approximately twofold to 13.3 p.p., pointing to a relatively even less open UK economy.

Moreover, given the importance of global value chains, less trade openness will impact commerce with all partners, not just those in the EU. Intermediate goods and services represent most of trade in advanced economies, and amounts to 2/3 of volumes between the EU and the UK. Higher trade barriers affect the costs of foreign supplies, reducing the competitiveness of UK-based production, and the ability of firms to participate in global value chains. The consequences will take time to materialize in full. Analysis conducted by the Office for Budget Responsibility (a government agency) suggests that, in the long run, Brexit will reduce trade openness by 15%, further widening the current difference of 13.3% with UK’s Euro Peers.

The uncertainty that resulted from the Brexit process and the loss of access to the EU Single Market have also taken a toll on business investment. The level of investment has stagnated and remains approximately unchanged since the Brexit referendum, underperforming its Euro Peers. The most conservative estimate of the negative effect of Brexit on the level of investment is 10% (and some are as high as 23%), which indicates a significant impact on the stock of capital and therefore long-term growth, even in the most optimistic scenarios.

Changes in foreign direct investment (FDI) explain part of the developments in total investment. In addition to the importance of FDI for growth and productivity, this is relevant because it reflects how the attractiveness of the UK has evolved over time. Since the 1990s the UK has historically been a top recipient of FDI flows, and reached a stock of FDI of over 2.3 trillion pounds (GBP), with more than half being from the EU. More recently, however, over the post-Brexit 2017-2021 period, the UK has fallen behind France and Germany in terms of FDI flows as a proportion of GDP

To summarize, years after its 2016 referendum decision to leave the European Union (EU), the UK continues to display subpar economic performance, which can be mainly attributed to the negative effect of new trade restrictions. This case study demonstrates that tariffs and non-tariff barriers, additional regulation and administrative costs, and other economic frictions lead to a misallocation of capital resulting in lower growth and productivity.

Download the PDF version of this weekly commentary in English or عربي