Global trade is widely considered a crucial metric for evaluating economic activity. In fact, few indicators can match the insights provided by trade data when it comes to gauging global economic conditions. Rooted in real cross-border transactions, trade data provides a comprehensive understanding of the overall demand for essential products and production factors. This includes physical goods, capital goods, as well as fundamental inputs, such as raw materials and commodities. As a result, global trade data is highly responsive to macroeconomic conditions, fluctuating in accordance with the cycles of economic expansion and contraction.

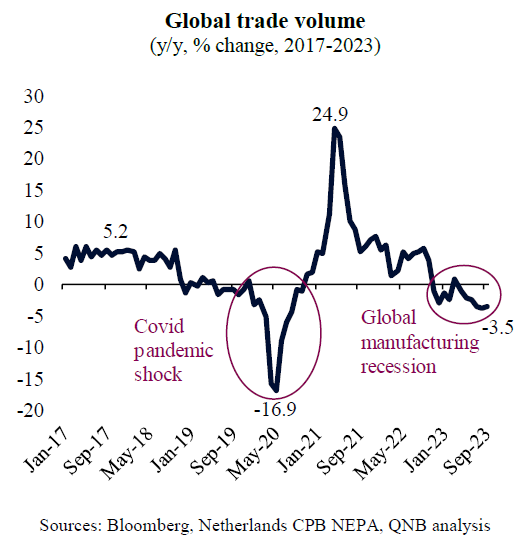

Recently, after the sharp rebound in activity following the pandemic, global trade showed significant weakness, contracting for several months. According to the Central Planning Bureau of Netherlands for Economic Policy Analysis (CPB NEPA), global trade volumes contracted by around 3.5% year-on-year (y/y) in September 2023, the latest data print available. Surprisingly, this has been taking place even as bottlenecks and supply-chain constraints continued to ease. This is likely associated with the ongoing global manufacturing recession, which depresses demand for goods, negatively affecting major manufacturing exporters, such as several Asian and European countries.

However, global trade volume data tend to give us a picture of the recent past rather than the present or incoming future. CPB NEPA data, for example, are released with a delay of three months. It is preferable to look at alternative data points that tend to provide coincident and forward-looking insights, rather than backward looking ones, i.e., leading indicators that anticipate what the economy is likely to do.

In our view, leading indicators are suggesting that the slump in global trade is likely over, even if there are no conditions for a significant recovery or boom over the coming months. Three main points support our analysis.

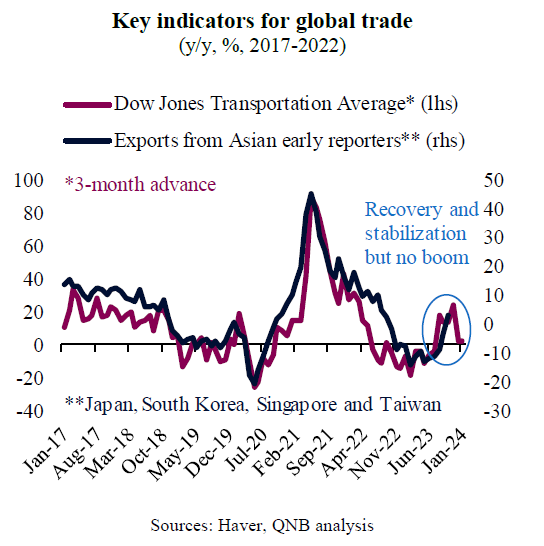

First, coincident indicators from early-reporting and highly open economies of East Asia (South Korea, Taiwan, Singapore, and Japan) are already suggesting an expansion. After more than a year in the doldrums, including double-digit declines for several months, exports started to expand again in October 2023. This is relevant, as these countries tend to lead global trade patterns, given the key role they play in the supply chain of large multinational corporations. Such movements indicate a significant stabilization and even modest recovery in overall global trade in Q4 2023, which should be sustained over the coming quarters, particularly after a long manufacturing recession.

Second, forward-looking investors are also anticipating an improving situation. Indeed, investor expectations about future earnings of the transportation sector, a key leading indicator for future growth in global trade, also continues to point to a recovery in the demand for physical goods. The Dow Jones Transportation Average, an equity index comprised of airlines, trucking, marine transportation, railroad and delivery companies, whose performance traditionally leads exports by at least 3 months, suggests a broad stabilization in trade over the coming months, even if signs for a more pronounced economic thrust are not found yet.

Third, foreign exchange (FX) movements are also likely to further play their part in supporting global trade. Historically, global trade is negatively correlated with the USD, with trade volumes expanding when the USD is down and vice versa. Despite some volatility earlier last year, the USD index is already down almost 9% from the highs seen in late September 2022. USD weakness is a major tailwind to global trade growth. Around 40% of global trade flows are invoiced in USD and a weaker USD makes non-US imports cheaper. This increases disposable incomes or even supports the substitution of domestic products for imports, positively affecting trade volumes.

All in all, we believe the conditions are given for global trade to stabilize further, potentially returning to modest growth. This is predicated in stronger coincident data, forward-looking expectations from transportation investors and more supportive FX movements. However, despite the stabilization, there are no indications for a sharper recovery over the coming months.

Download the PDF version of this weekly commentary in English or عربي