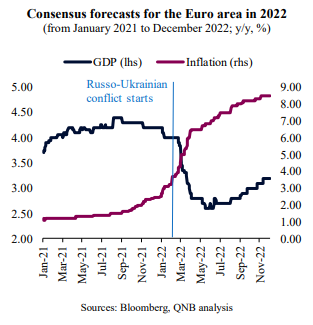

Euro area growth prospects have been particularly volatile in recent quarters. The region has rapidly transitioned from a post-pandemic re-opening to a “crisis-driven economy” following the beginning of the Russo-Ukrainian conflict. In fact, Bloomberg consensus forecasts for Euro area GDP growth in 2022 were rapidly adjusted after the Ukraine War started from above 4% to below 3% in a matter of months, with the prospects of a deep and lasting recession at end 2022 and beginning 2023.

There are indeed few precedents to the magnitude, breadth and depth of the negative shocks that affected the region. On the supply side, the legacy of pandemic-related disruptions was amplified by the most significant energy crisis in decades. The geopolitical spillovers from the Russo-Ukrainian conflict materialized with embargoes, sanctions and trade bans, negatively affecting European utilities as well as energy intensive industries. On the demand side, the otherwise strong momentum from the post-pandemic economic re-opening started to falter, as high and rising inflation depleted disposable incomes, which dampened consumer and business sentiment.

As a result, the Euro area was severely hit by a difficult combination of low and slowing growth with high and rising inflation.

Consensus forecasts for the Euro area in 2022

However, despite the challenges, the Euro area has so far proven to be more resilient than most analysts anticipated, particularly the ones expecting a deep and lasting recession. In this article, we dive into the three factors that explain the resilience of the Euro area economy.

First, the Euro area has outperformed expectations consistently in recent months, with data prints still pointing to a robust and expanding economy. In fact, the region has grown by 4% and 2.1% year-on-year in Q2 and Q3 2022, respectively, beating most forecasts. The strong performance was underpinned by private consumption expenditure, a strong summer season for tourism and services as well as a post-Covid inventory build-up. Moreover, while higher frequency activity data, such as the Purchasing Managers’ Index, has been weakening for months, it is starting to show the first signs of stabilization. This suggests that the underlying fundamentals of the European economy before the geopolitical shock were stronger than previously thought, particularly when it comes to the labour market and household consumption.

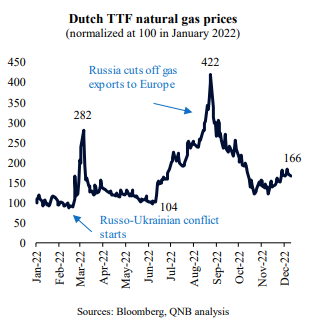

Second, prospects for the European energy crisis this winter have improved significantly, allowing for more stable industrial production and less stringent utility consumption. Positive developments so far are associated with a milder than average winter, more effective energy saving mechanisms, high gas inventories from last summer and steadier regional energy output. Importantly, Dutch TTF natural gas prices, the benchmark for Europe, have reversed most of the advance from the historical spike that started during the summer, when Russia announced it would no longer export gas to Europe via the Nord Stream pipeline. More affordable gas prices provide some relief for both households and governments, due to lower utility costs as well as reduced fiscal commitments for energy subsidies, boosting disposable incomes.

Third, the policy set up also favours a floor for Euro area growth this time. In contrast to previous economic crises in the Euro area, there is little fundamental division about potential support measures in case new risks materialize. There is little appetite for too much fiscal discipline, as even countries that historically presented persistent budget surpluses, such as Germany, Austria and the Netherlands, are now presenting deficits. This is due to the need to fund energy subsidies and direct transfers to cash-strapped households, utilities and corporates. In other words, fiscal deficits are now commonplace across the Euro area. Hence, there is a consensual understanding about emergency fiscal measures or even emergency support from the European Central Bank (ECB). This should therefore provide the needed institutional backstop for additional policy action whenever needed.

All in all, the economic challenges are salient and the outlook is still rather difficult for the Euro area. A regional recession for the Q4 2022-Q1 2023 period is almost a given. However, the deep downturn expected by some analysts should be avoided. Resilient fundamentals, a more manageable energy crisis during this winter and more policy cohesion offer some relief and support. This should allow for a 0.5% Euro area GDP expansion in 2023.

Download the PDF version of this weekly commentary in

English

or

عربي