The US Federal Reserve (Fed) had a busy year in 2019. After a long and gradual process of monetary policy tightening in 2015-2018, the Fed undertook a major policy reversal with the so-called “dovish pivot” of 2019. The most discussed element of such a turn was the sudden change in the direction of policy rate action. While forward guidance in late 2018 pointed to two policy rate hikes in 2019, the Fed delivered three 25 basis points policy rate cuts for the year. But policy change did not concentrate only on policy rate action. The Fed has also dramatically changed its stance on quantitative measures, from quantitative tightening (QT) and balance sheet “normalization” to continuous rounds of significant balance sheet expansion. Our analysis delves into the balance sheet side of recent Fed policy changes, highlighting their importance for liquidity provision.

Under the existing US monetary policy framework, the primary policy tool is the target range of the federal funds rate, which is actively adjusted in order to stimulate both inflation and employment to move towards the Fed target. In normal circumstances, the Fed does not have specific quantitative targets. But circumstances changed in the aftermath of the great financial crisis of 2007-08, when quantitative measures became relevant, especially in the form of quantitative easing (QE) or large scale asset purchase programs.

QE programs are unconventional monetary policy tools that were recently waged after the great financial crisis, when policy rates quickly reached nominal levels at or close to zero. Operationally, QE is the extraordinary process through which central banks intentionally expand their balance sheets beyond normal levels. QE implementation by the Fed required the systematic acquisition of a number of government and government-backed fixed income securities from the secondary markets against bank reserves. The aim was to remove long-term government papers from the market, placing additional downward pressure on rates and pushing investors towards riskier securities, further easing financial conditions.

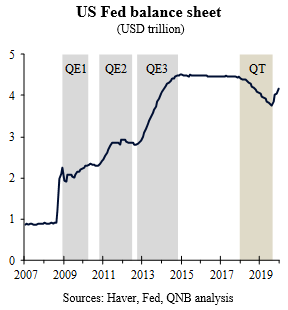

The Fed launched three QE programs since the Lehman Brothers collapse in 2008. With QE1, QE2 and QE3, the Fed’s balance sheet expanded by around USD 3.6 trillion (Tn) from USD 900 billion (Bn) to USD 4.5 Tn. In the process, the economy recovered and staged the longest expansion cycle ever recorded. But the search for a “new Fed’s balance sheet normal” became an uncertain exercize. Tighter financial regulation and operational changes in monetary policy implementation made it more difficult to gauge what would be the ideal size of the Fed’s balance sheet or the optimum level of bank’s reserves. In a trial and error basis, QE tapering started in 2014 and QT started in 2017. Under QT, the Fed’s balance sheet slowly contracted by more than USD 600 Bn as maturing assets were not replaced by new securities.

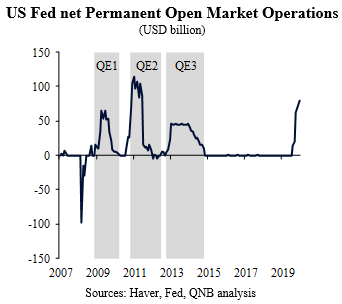

Market reactions to QT, including the cash scarcity that prompted the Repo spike in September 2019, suggested that the shrinkage of the Fed’s balance sheet went too far. The Repo tantrum signalled that money markets needed more liquidity and that QT needed to be not only stopped but reverted. Since then, the Fed’s response to actual or potential money market disruptions was swift, including both temporary and permanent open market operations. The magnitude of the response is sizable, with permanent net purchases of securities amounting to about USD 250 Bn in the last four months.

In our view, the Fed’s decision to go beyond temporary open market operations is correct. Recent experiences have proven that, under current economic conditions, money markets can only properly function if the Fed secures a permanent increase in the supply of funds to repo markets. As such, appropriate liquidity provision demands an expansion in both the Fed’s balance sheet and banks’ excess reserves. All in all, we believe that the Fed will continue to expand its balance sheet well into H1 2020, which should further support the upcoming re-acceleration of US and global growth.

Download the PDF version of this weekly commentary in English or عربي