The resilience of the US economy has driven a dramatic shift in its growth expectations. During the first half of last year, the outlook for 2024 reflected widespread pessimism given significant headwinds. These headwinds included a high rate of inflation that eroded the purchasing power of households, disruptive commodity markets, and the record monetary policy tightening cycle by the Federal Reserve Board. A recession seemed almost inevitable, and the discussions regarding the macroeconomic outlook centered on balancing the prospects of a “hard” or a “soft” economic landing.

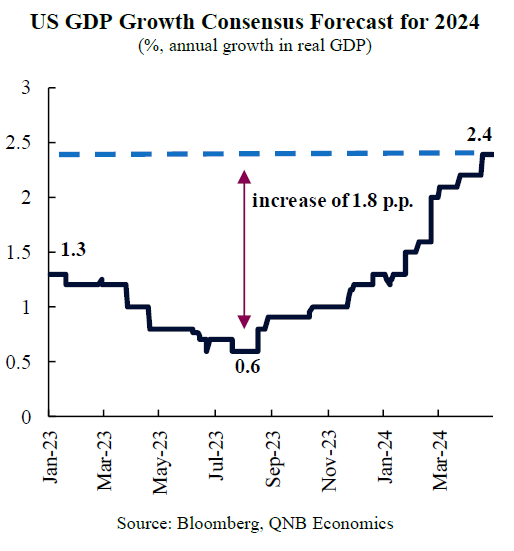

The Bloomberg survey consensus is a useful tool that reveals market expectations and the evolving views over major macroeconomic developments. This benchmark survey tracks forecasts from analysts, think tanks, and research houses, presenting a range of projections, as well as the median point of market expectations. In July last year, the consensus for growth of the US economy in 2024 reached a low of 0.6%. Then, it began a steady upward trend, and increasead by a remarkable four-fold to 2.4% this year, on the back of better-than-expected economic indicators, including a surprisingly strong print for GDP for the last quarter of 2023. This suggests that the economy remains in good standing, and would decelerate gradually relative to the 2.5% expansion of 2023.

In this article, we analyse the evolution of three key production sectors, and their leading indicators, that underlie the resilience of the overall economy and its gradual deceleration.

First, the service sector has remained robust following the post-Covid pandemic normalisation. The GDP figures for the first quarter of this year showed that consumption of services grew at a outstanding annualized rate of 4%, significantly above the yearly expansion of 2.3% in 2023.

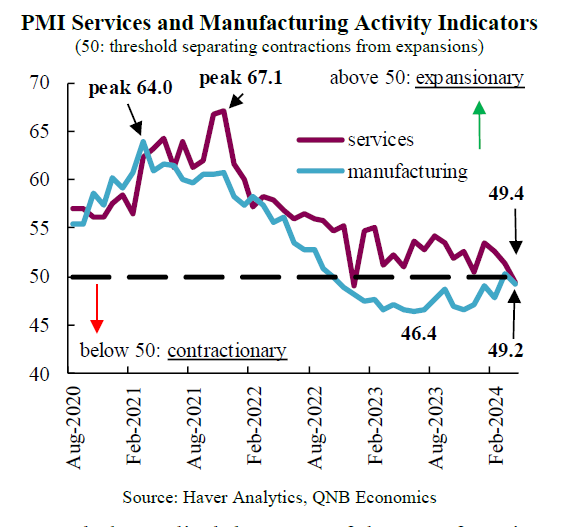

The most recent prints of the Purchasing Managers Index (PMI) signal that the outlook remains stable. The PMI is a survey-based indicator that provides a measurement of improvement or deterioration in economic activity. An index level of 50 serves as a threshold that separates contractionary (below 50) from expansionary (above 50) business conditions. The PMI for the service sector reached a peak at 67.1 in November 2021, as the sector recovered vigorously from the low at the beginning of the Covid-pandemic. Since then, this indicator has moderated at a soft pace, fluctuating above or close to the 50-point mark that indicates expansion. The performance of the service sector provides support for the economy, as it accounts for over 70% of overall activity.

Second, the cyclical downturn of the manufacturing sector has reached its bottom, and the sector transitions towards a phase of recovery. During the Covid-pandemic, household consumption of goods rocketed abnormally above its trend, due to lock-downs and restrictions that disrupted normal spending behaviour away from services. After reaching its peak of 64 in March 2021, the manufacturing PMI began a downward trend, as spending in goods gradually decelerated with the normalisation of spending patterns. The manufacturing PMI entered the contractionary range at the end of 2022, but steadied in the second half of 2023, and exceeded the 50-point mark into expansionary range in March this year. Although the strength of this recovery is still to be determined, the end of the downturn in the manufacturing sector is providing additional backing to the economy.

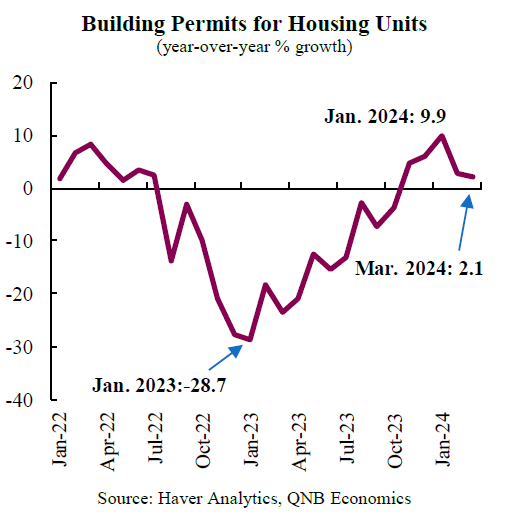

Third, the construction sector has stabilised after a period of contraction. Last year, higher interest rates and tighter lending standards by banks had increased borrowing costs and reduced the availability of credit, resulting in a negative impact for construction. Key indicators of the construction sector, such as building permits and new housing starts, were contracting at rates of more than 20% in year-over-year terms. The sharp retrenchment in some of the indicators raised the alarms, given that negative growth rates of this magnitude had historically anticipated recessions. By the end of 2023 many indicators had stabilised, and major gauges such as building permits, new housing starts, and median sale prices have improved in inter-annual terms, suggesting that construction activity will no longer be a drag on the overall economy.

All in all, data from key economic sectors signal that growth in the US economy is stabilizing, and a deceleration will be gradual. In our view, in spite of interest rates remaining higher for longer, it is unlikely that a recession will take place in the US this year, even if household consumption upsets the current optimistic growth expectations.

Download the PDF version of this weekly commentary in English or عربي