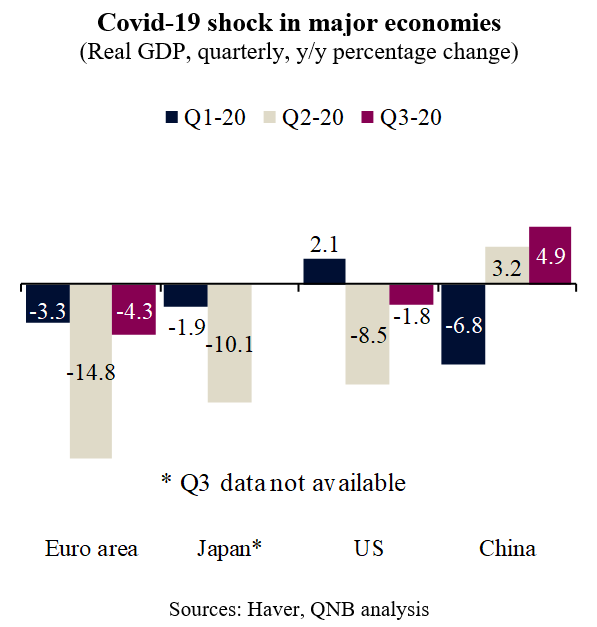

Over the last few months, aggressive policy stimulus and the partial containment of the Covid-19 pandemic in large advanced economies produced a significant reversal of global trends. In fact, in Q3 2020, after a sharp but deep global depression, a broad-based economic stabilization took place. While activity was still far from pre-pandemic levels and even in contraction territory on a year-over-year basis in all major economies except for China, the rate of change improved significantly and the positive momentum created optimism and hope.

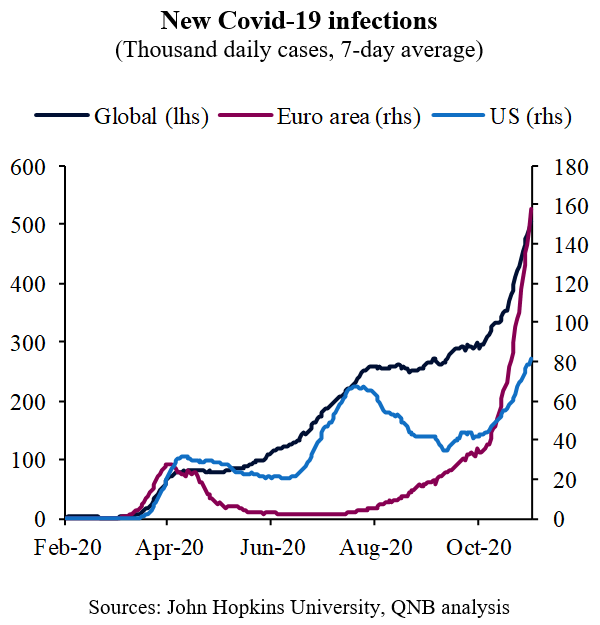

But conditions are taking another dramatic turn for the worse in large advanced economies. A “second wave” of new Covid-19 cases is emerging, particularly in the Euro area and the US. After months of decline and stabilization in the number of new Covid-19 infections, the epidemic is now not only worsening in several advanced economies but also showing signs of a steep acceleration ahead of the flu season on the Northern Hemisphere.

Importantly, several European countries (France, Germany, Belgium, Greece, Spain, the UK, Italy) are moving again towards more aggressive mitigation strategies, including the re-imposition of hard social distancing measures such as quarantines, curfews and lockdowns. The objective is to lengthen the time through which the virus spreads over the winter, flattening the curve of infections before hospitals get overloaded by a bigger surge of severe cases. The aim is to save lives, increase recovery rates and avoid unintended consequences associated with strained healthcare systems.

But a “second wave” of hard social distancing measures will come with costs to large advanced economies, potentially de-railing the economic stabilization process that started in Q3 2020 with a “double dip recession” or “stop-and-go” activity patterns. This piece dives into three key points about the economic consequences of a “second wave” of severe epidemics in the Euro area and the US, drawing parallels with the “first wave” early in the year.

First, this time around there is less uncertainty about the virus itself and how to handle it. Health authorities understand more about the virus and its transmission, and treatments have improved across the board, with some data suggesting that hospitalization and death rates are diminishing. Moreover, there is more expertise now on how to implement social distancing measures as well as on how to manage its economic consequences. Financial support facilities to corporates and households were already introduced and can be extended further in the coming months in the Euro area and the US.

Second, supply side effects are expected to be smaller than in the first wave, producing a more moderate shock to activity. This is because social distancing mandates are slightly less stringent than before and because work-from-home infrastructure is already in place. To a certain extent, a large part of the economy in the Euro area and the US is already adapted to functioning under the “new normal” with the pandemic.

Third, economic stimulus will likely need to be even more aggressive or generous than in the first lockdown, particularly when it comes to support to the corporate sector in large advanced economies. In the first wave, vulnerable industries received the majority of their support line in the form of concessional loans and delayed payments of taxes. A simple extension of those schemes would lead to very high levels of private debt, potentially causing a wave of bankruptcies in the Euro area and the US. New financial support measures need to be designed for the “second wave.”

All in all, several large advanced economies were unable to achieve an orderly transition from horizontal social distancing (government mandated lockdowns of entire populations and regions) to vertical social distancing (voluntary precautions and the isolation of the most vulnerable and the infected patients). This will slow down the process of economic normalization, likely producing a double dip global recession. However, this should be a rather short global recession, probably concentrated on Q1 2021. After the Northern Hemisphere’s winter season, and with the global efforts for a vaccine bearing fruit, the global economy should experience a full-fledged, rapid economic recovery.

Download the PDF version of this weekly commentary in English or عربي