The global macro environment is presenting some of the most challenging conditions in generations. Rare macro distortions, such as the combination of high inflation and slowing activity, are quickly creating bouts of significant market dislocation and stress. This can be observed across most asset classes and jurisdictions.

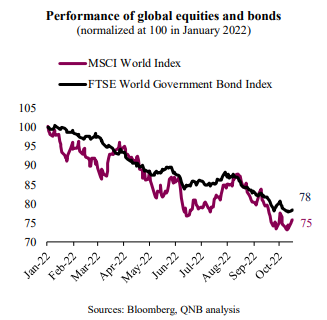

As central banks hike interest rates to combat high inflation, the attractiveness of cash versus other types of assets increase. This creates downward pressure in the overall value of both equities and bonds. In fact, the global asset sell-off that prevailed throughout the year deepened in recent months. Year to date (YTD), global bonds and equities are down 22% and 25%, respectively.

These market moves produced significant drawdowns in balanced portfolios of investors that are used to benefiting from stable positive returns. According to Bank of America, the YTD return so far of a traditional asset allocation strategy that splits the portfolio into 60% equities and 40% bonds is presenting the worst yearly performance in a century. In other words, we are witnessing this year the largest and fastest financial wealth destruction process ever seen. The damage is becoming so salient that financial stability concerns are coming to the fore.

Monetary authorities in the UK had to backstop the local bond market amid a historic rout in late September. As long-term yields spiked to 20-year highs above 5%, UK bond prices collapsed. This caused leveraged pension funds to the brink of insolvency after a wave of margin calls forced them to liquidate their bonds. The Bank of England therefore announced it would intervene in “whatever scale is necessary” to calm markets. This required large-scale purchases of bonds.

The UK episode opened the discussion about financial instability and the potential need for financial backstopping from other central banks as well. In mid-October, US Federal Reserve (Fed) officials engaged with institutional investors, bankers and financiers to understand the risks of UK-like market blowouts in the US. Similar discussions also took place in Europe.

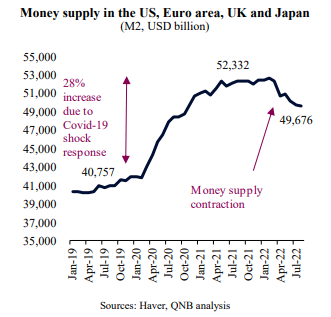

Importantly, these discussions are happening while major central banks are withdrawing balance sheet support from bond markets. Monetary authorities have been moving away from balance sheet expansion towards a more neutral or even restrictive balance sheet position. The US Fed started last month its maximum balance sheet reduction pace of USD 95 Bn per month. This implies a significant demand reduction for bonds, which pushes yields up across different tenures and drains money supply.

In our view, it is likely that major central banks will have to decouple their interest rate policy normalization from the balance sheet reduction measures. Inflation is too high and this threatens the credibility of monetary authorities, given their inflation mandate. In the past, most central bankers believed in the need for an alignment of policy tools, i.e., policy rates and balance sheet should be pointing to the same direction or at least not contradicting each other – easing, neutral or tightening. This led to the playbook of combining policy rate hikes with balance sheet stability or reduction, in contrast to balance sheet expansion, which increases money supply and liquidity in the system.

Despite such past practice and beliefs, we are of the opinion that current conditions require a differentiated approach in the application of monetary policy tools for major central banks: interest rate policy should be the main tool to combat high inflation while balance sheet policy should be adjusted, in a targeted matter, to potentially backstop stressed asset markets. This would allow for a more orderly and sustainable process of monetary policy adjustment.

Download the PDF version of this weekly commentary in

English

or

عربي