After a strong economic recovery from the 2020 pandemic shock, select frontier markets in Sub-Saharan Africa benefited from the “great global re-opening” in 2021 and 2022. The end of major, persistent lockdowns or other strict social distancing measures in SSA allowed for a pick up in activity and a rebound in domestic consumption, fueling a regional economic expansion.

However, the tailwinds from the re-opening started to fade over the last couple of quarters and can now be offset by headwinds from global conditions, particularly as global growth decelerates further, commodity prices are kept elevated and major central banks continue to hike policy rates. Higher import bills and tighter international financial conditions often pressure the external balances of vulnerable frontier markets. Hence, it is ever more important to track different measures of external vulnerability in key Sub-Saharan African (SSA) economies.

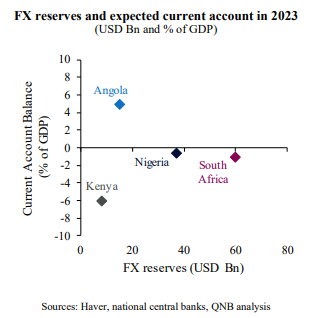

We assess external vulnerability along two dimensions: the current account balance and the overall level of official foreign exchange (FX) reserves. Countries that run current account deficits need to finance it with either foreign capital or drawing down their own FX wealth. During challenging times, when global economic or financial conditions are difficult, capital flows can dry up or reverse, making it even more difficult to fund deficits without drawing down FX assets. That is why current account balances are an important metric to assess the exposure of countries to capital flows and risk sentiment. The below graph delineates the level of FX reserves versus the expected 2023 current account deficit for key SSA economies.

Our analysis delves into the current account position and FX reserves of the four largest frontier or emerging economies in SSA, namely Nigeria, South Africa, Angola and Kenya, drawing conclusions about their resilience against potential global or regional shocks.

Divergence in external vulnerability across the largest SSA economies are currently mostly explained by each country’s status as a net commodity importer or exporter. Net commodity exporters, such as Nigeria and Angola, tend to either have accumulated more FX reserves over time or presented current account surpluses. In contrast, net commodity importers, such as South Africa and Kenya, present a less benign external position.

Nigeria’s current resilience is underpinned by strong commodity markets globally. The country is the largest oil exporter of SSA and a major exporter of agricultural products, such as cocoa, rubber and palm oil, as well as solid minerals, such as tin and limestone. Elevated commodity prices continue to support the funding of the country’s growing imports, even as productivity remains low and structural reforms are not implemented at an optimal pace and level. Nigeria amassed USD 37 Bn in official FX reserves, which comfortably covers the USD 4 Bn of current account deficits expected for this year.

While Angola’s level of FX reserves is relatively low at USD 14 Bn, the country is expected to run a current account surplus of about USD 7 Bn in 2023. This is due to the booming oil exports. Elevated oil prices are providing Angola with a windfall in revenue. This allows the country to invest at a reasonable rate and potentially even build up more FX reserves over the next several quarters.

South Africa is a net external borrower, which means that it runs current account deficits. While South Africa is a known exporter of key commodities, such as gold, platinum, coal, iron ore and diamonds, this is more than offset by the need to import other commodities, particularly oil and food-related products. Hence, the country’s terms of trade have been deteriorating, placing economic authorities under pressure. The only large SSA country that is considered an emerging rather than frontier market, South Africa is more vulnerable to foreign investor sentiment and has been hit by tightening global financial conditions and FX turbulence. South Africa’s official reserves amount to USD 60 Bn. While this more than covers for the USD 4 Bn current account deficit expected for this year, it only covers about 60% of the country’s short-term external debt.

Kenya is another net external borrower, running structural current account deficits for years. Conditions deteriorated in recent quarters as its import bills ballooned with higher energy prices, which could not be offset by its exports of textile manufacturing, tea, coffee and horticultural products. The country is under pressure and will need to enact significant re-balancing measures to avoid a more acute balance of payment crisis. This will likely require some import compression and lower GDP growth. Kenya’s FX reserves are limited at USD 8 Bn, barely covering the expected current account deficit of USD 7 Bn.

All in all, while SSA economies are still vulnerable, global trends, such as elevated and sustained commodity prices despite higher interest rates, could benefit SSA net commodity exporters going forward, strengthening their resilience towards further economic volatility and shocks. On the other hand, these same trends will continue to further increase the vulnerability of SSA net commodity importers.

Download the PDF version of this weekly commentary in English or عربي