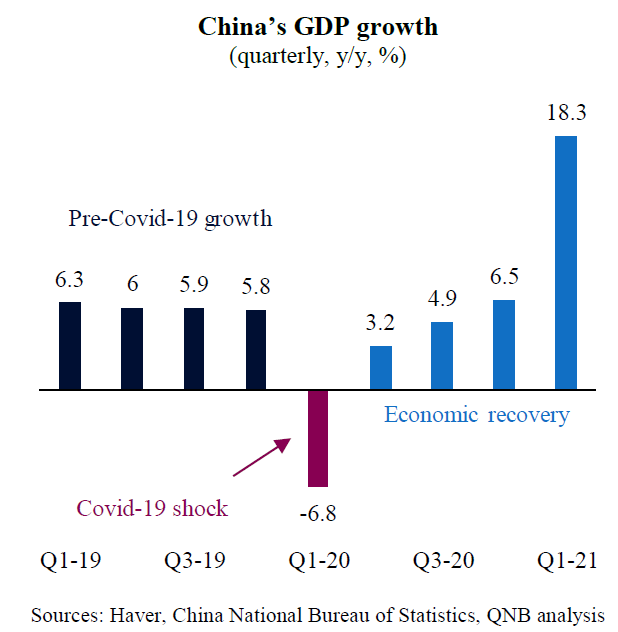

China continues to show a strong economic performance in the wake of the Covid-19 pandemic. The positive momentum came after a sudden economic collapse in Q1 2020, when the country experienced the first year-on-year (y/y) GDP contraction in decades, on the back of Covid-19-related lockdowns and other social distancing measures.

China’s economic strength can be explained by an effective management of the pandemic, robust global demand for electronics and powerful policy stimulus. According to the China National Bureau of Statistics, China’s GDP grew by 18.3% y/y in Q1 2021, marking the fourth consecutive quarter of economic expansion within the recovery. This piece dives into three key points associated with recent Chinese economic activity.

First, while China’s GDP growth in Q1 2021 was seemingly extraordinary, it was propped up by “base effects,” i.e., it was unusually high due to the low base for comparison in Q1 2020, when the pandemic-induced economic collapse took place. If considered on a sequential quarter-on-quarter basis instead of y/y basis, the economy printed a more moderate 0.3% expansion. This is still a positive development, but far from what a two-digit y/y growth figure would normally suggest.

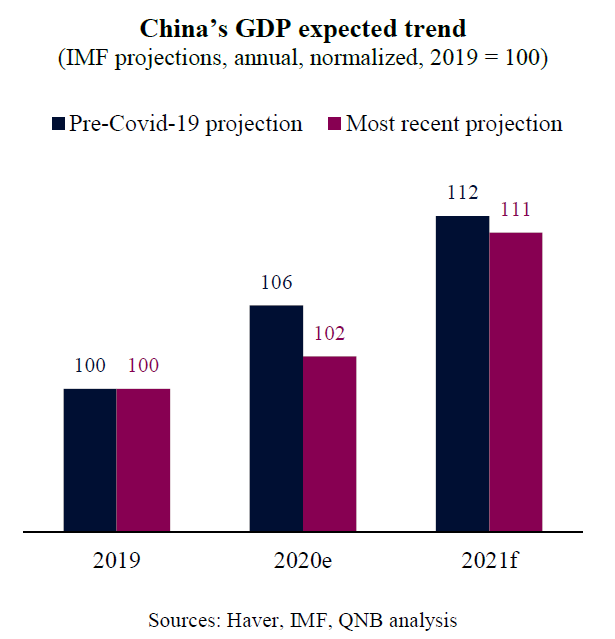

Second, despite the unprecedented Covid-19 shock last year, the Chinese economy is on track to re-gain lost ground. As an example, in October 2019, the IMF expected that the Chinese GDP would have grown by 12% from that year to the end of 2021. Such projection did not account for the massive exogenous “black swan event” shock that emerged with the pandemic. However, given China’s fast recovery, even with the pandemic, the country’s GDP is now expected to grow by 11% from 2019 to 2021. In other words, by the end of this year, China is expected to be only 1% away from the pre-pandemic GDP trend. This is an extraordinary achievement as most advanced and emerging economies are likely going to take years to return to even pre-pandemic GDP levels, not to mention a potential catch up with the pre-pandemic GDP trend.

Third, despite the economic recovery in recent quarters, Chinese domestic private consumption remains weak. This suggests that post-Covid-19 growth is still over-reliant on state-induced, credit-intensive infrastructure investments. While public investments may have been important to support the economy during the pandemic, they are not expected to be a sustainable source of long-term growth. China’s infrastructure is already highly developed and additional investments in the sector tend to be less efficient, often contributing to create inadequate levels of indebtedness and overcapacity. Economic authorities are therefore looking to promote “higher quality” growth drivers in the future, focusing on consumption, tech exports and private business investments.

All in all, China is once again proving that its economy is extremely resilient to exogenous shocks. The recovery is now well under way and GDP is expected to grow by 8.6% this year.

Download the PDF version of this weekly commentary in English or عربي