After a strong economic recovery from the temporary collapse produced by the Covid-19 pandemic, emerging markets (EM) benefited from a much more benign global macro environment. However, recent gains can partially reverse should major risks materialize, especially if the global recovery weakens or if a “great Asian re-opening” is further delayed by new virus variants and low vaccination rates. New bouts of pressure on external balances of vulnerable EM would be expected to follow any sudden change in global or regional risk sentiment. Hence, it is ever more important to track and analyse different measures of external vulnerability in those markets.

We assess external vulnerability along two dimensions: the current account balance and the overall level of official foreign exchange (FX) reserves. Countries that run current account deficits need to either finance it with foreign capital or drawdown their own FX wealth. During challenging times, when global conditions are difficult, capital flows can dry up or even reverse, making it difficult to fund deficits without drawing down FX assets. That’s why current account balances (as a % of GDP) are an important metric to assess the exposure of countries to capital flows and risk sentiment.

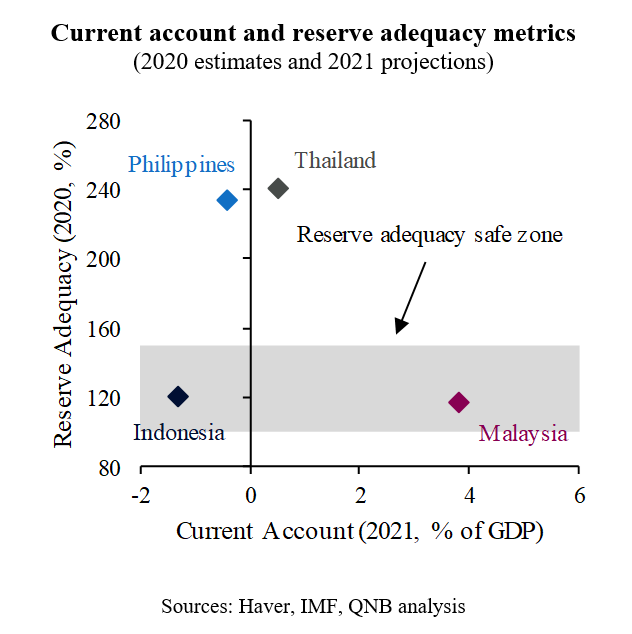

Official FX reserves can be an important backstop to absorbe external shocks. But different countries have different FX reserve needs. Traditionally, a country’s FX reserves are considered within adequate levels whenever they range above 3 months of imports and they are enough to cover for 20% of the overall volume of local currency held by the public or at least for a full year of external debt obligations. The International Monetary Fund (IMF) created a useful composite indicator for such measures, called the IMF reserve adequacy metric. Countries are deemed to hold adequate levels of FX reserves whenever they can cover the 100-150% threshould of the IMF metric.

Our analysis delves into the current account position and FX reserves of the four large emerging economies of the Association of Southeast Asian Nations (ASEAN), namely Indonesia, Thailand, Malaysia and the Philippines, drawing conclusions about their resilience against potential global or regional shocks.

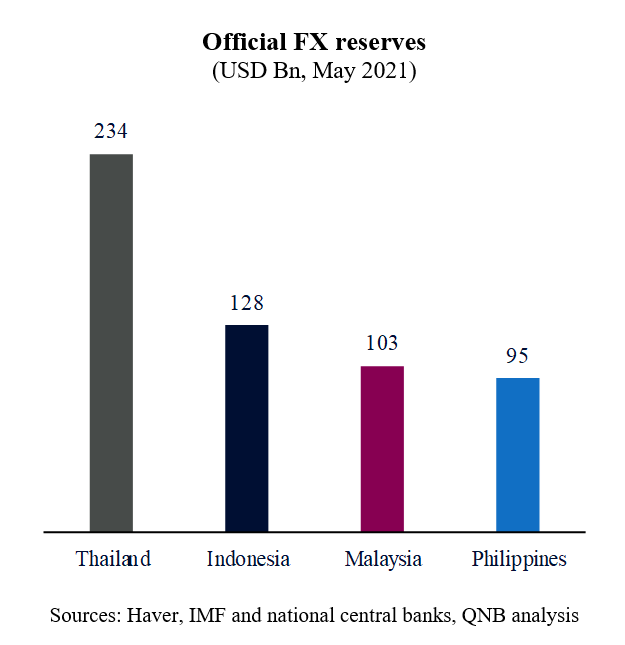

Despite a high exposure to the global economic cycle (manufacturing exports and tourism), Thailand is still in a good position to weather sudden changes in capital flows. The country had run sizable current account surpluses for years and is expected to present a healthy surplus in 2021. Even with large parts of its sizable tourism industry still shut down for foreigners and with terms-of-trade deteriorating on the back of stronger commodity prices, the situation appears stable. Thailand has amassed USD 234 Bn in official FX reserves, which comfortably covers 241% of the IMF reserve adequacy metric.

Malaysia, a big producer of manufacturing goods and commodities, is another resilient ASEAN economy. Like Thailand, the country had also run persistent current account surpluses for years. As a net oil and soft commodity exporter, Malaysia has been positively affected by the recent strength of commodity markets, which resulted in a bigger current account surplus. Malaysia’s reserve adequacy metrics are much tighter than those for Thailand, with the central bank holding less than half of the amount of FX reserves that Thailand holds at USD 103 Bn. However, Malaysia is still in the safe zone of the IMF reserve adequacy metrics with a 118% coverage.

The Philippines is a net external borrower, which means that it runs current account deficits. With a large trade deficit that is currently only partially offset by sizable inflows of remittances from the community of Philippine expatriate workers, the country is expected to run a current account deficit that amounts to 0.4% of GDP. However, the deficits are mostly driven by a healthy push for much needed investment, and monetary authorities control ample FX reserves. Official reserves of USD 95 Bn cover 234% of the IMF reserve adequacy metric.

Indonesia is the most exposed large ASEAN country to potential external shocks. It runs persistent current account deficits on the back of both fiscal imbalances and external borrowing from the non-financial corporate sector. When compared to the other large ASEAN countries, Indonesia’s sensitivity to international capital flows is amplified by a significant currency mismatch, i.e., the fact that a large share of the debt from the public and corporate sectors are denominated in USD, even though a significant part of their revenues or earnings are in local currency. But it is not all doom and gloom. Indonesian official FX reserves amount to USD 128 Bn, covering 121% of the IMF reserve adequacy metric.

All in all, large ASEAN economies are relatively resilient to sudden changes in risk sentiment and capital flows. Such resilience is a major source of support in a context of higher uncertainty associated with the slowdown of the global recovery and potential flare ups from new Covid-19 variants. Buffered by moderately strong external positions, the ASEAN economies are in a better shape to navigate potential global shocks than the majority of other EM.

Download the PDF version of this weekly commentary in English or عربي