Inflation and GDP growth are the two most powerful drivers in a modern economy. Although in different ways, they both affect all major decisions about when or where to consume and invest. An ideal macroeconomic environment would combine high growth with low inflation, i.e., a rapid expansion of activity alongside stable prices. However, this “sweet spot” between growth and inflation is difficult to achieve, due to a historical positive correlation between them over the long-term. More growth tends to lead to full employment and capacity utilization, pressuring resources and prices.

Over the last several decades, from 1990 to 2020, the global economy thrived under a macro regime that is often dubbed as the “Great Moderation,” i.e., a period in which advanced economies benefited from moderate growth and low inflation. The “Great Moderation” was fuelled by several secular or long-term trends, including digitization, globalization, just-in-time manufacturing and independent central banks.

While digitization increased efficiency and productivity across countries, globalization opened new markets and allowed for a much larger working force to engage in value generating activities. To some extent, globalization came hand-in-hand with the “geopolitical dividend” brought up by the end of the Cold War (1947-1989) and the opening up of the great Chinese market. This was amplified by advances in supply-chain management and transportation infrastructure, which favoured a just-in-time global manufacturing network that operates with low inventories and fast deliveries. Under this network, production is optimized to respond to demand at a high frequency and the utilization of time, labor and materials are minimized. On top of this, the deflationary trends were also supported by institutional reforms and the operationalization of independent central banks that concentrated their activities in maintaining stable prices.

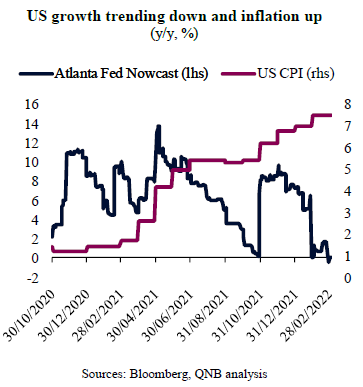

However, with the exception of digitization, the other trends that supported the “Great Moderation” peaked just before the Global Financial Crisis in 2008-09 and seem to be reversing sharply after the two great shocks of the 2020s: the Covid-19 pandemic and the Russo-Ukrainian conflict. After a period of strong recovery following the depths of the sharp downturn from the pandemic in 2020, there are increasing signs that the global macro picture is gearing towards a much less benign environment with low growth and high inflation. This economic phenomenon is called “stagflation”. In the US, still the leading force of the global economy, inflation is accelerating to a 40-year high, while, at the same time, high frequency indicators point to a sharp slowdown in activity. In fact, the Atlanta Federal Reserve “nowcast,” a running estimate of real GDP growth based on available economic data, points to a stagnant US economy. This will likely spill over to other economies, spurring a period of global “stagflation.”

Importantly, “stagflation” may not be only a temporary phenomenon associated with pandemic-related supply bottlenecks and geopolitical shocks. Two major changes suggest that global “stagnationary” forces may prevail for a longer period of time beyond the current cycle.

First, political relations among global super-powers are deteriorating rapidly, transforming the “geopolitical dividend” of global integration into a “geopolitical recession” of de-globalization. Examples include the US-China strategic rivalry and the recent sanctions against Russia, following the invasion of Ukraine. This contributes to reverse globalization and undermines just-in-time manufacturing, prompting an agenda of protectionism, supply-chain “onshoring,” food security and more closed border for migration flows. Moreover, it also makes the global economy more vulnerable to negative supply side shocks, such as the disruption in commodity markets triggered by the Russo-Ukrainian conflict. Hence, the “geopolitical recession” is negative for productivity, trade and investment flows, increasing production costs. This creates the conditions for lower growth and more elevated prices over the long-term.

Second, the pandemic has again led to a significant increase in global debt, which was already at its all time highs. Debt levels in major economies are too high and this makes them too sensitive to a more meaningful cycle of rate hikes. In this sense, should high inflation continue for longer, the magnitude and pace of monetary policy normalization would be more contained in order to avoid credit tantrums and potential recessions. In other words, high debt levels are forcing major central banks to moderate their inflation mandate in the name of credit and employment stability. Despite the “hawkish” pivot from major central banks in recent months, there is limited monetary policy room for a more comprehensive fight against inflation. Over time, this will contribute to persitent inflationary pressures.

All in all, the Covid-19 pandemic and the Russo-Ukrainian conflict may become catalysts to a long-term reversion of the features of the “Great Moderation,” producing a longer period of “stagflation.” This would endanger all the efforts of fiscal and monetary policy that were undertaken during the pandemic, prompting growth to reverse to pre-pandemic levels.

Download the PDF version of this weekly commentary in English or عربي