Global trade is often referred to as a key barometer of economic activities across countries. In fact, few indicators reflect the overall health of the global economy as well as trade data does. Underpinned by real cross-border transactions, trade data captures the demand for key products as well as production factors, including physical consumer goods, capital goods, basic inputs and commodities. As a result, global trade data tends to be highly sensitive to macro conditions, moving along with the cycles of economic expansion and contraction.

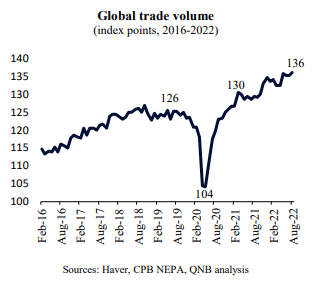

Recently, after the sharp but short-lived collapse in activity following the onset of the pandemic, global trade rebounded strongly. According to the Central Planning Bureau of Netherlands for Economic Policy Analysis (CPB NEPA), global trade volumes surged by more than 30% since the depths of the Great Pandemic Downturn in early 2020, far surpassing pre-pandemic levels and comfortably reaching all-time highs. Surprisingly, this has been taking place even as bottlenecks and supply-chain constraints persisted.

However, global trade volume data tends to give us a picture of the recent past rather than the present or incoming future. CPB NEPA data, for example, are released with a delay of three months, which means that their recent print reflect trade volumes from August 2022. It is preferable to look to alternative data points that tend to provide forward looking insights, rather than backward looking ones.

In our view, leading indicators are suggesting that global trade will not continue to grow but slow down and even contract for a few months. Three main points support our analysis.

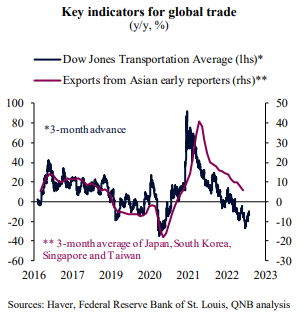

First, high frequency data from key major economies (US, Euro area and Japan) are pointing to a “global trade recession.” The flash Purchasing Managers’ Index (PMI) surveys from advanced economies printed consecutive months of slowdown in new export orders which slipped further into contractionary territory in October. High inflation is negatively affecting disposable income across major economies, dampening overall demand. This is in line with a continued deceleration of trade growth in early reporting Asian exporters (Japan, South Korea, Singapore and Taiwan). These countries tend to lead global trade patterns, as they play a key role in the supply chain of manufacturing activities across continents.

Second, forward-looking investors are also anticipating a significant contraction. Indeed, investor expectations about future earnings of the transportation sector, a key leading indicator for future growth in global trade, is indicating a sharp contracting in demand for physical goods. The Dow Jones Transportation Average, an equity index comprised of airlines, trucking, marine transportation, railroad and delivery companies, whose performance leads global exports by at least 3 months, peaked in March 2021, declining rapidly ever since to deep contraction rates.

Third, foreign exchange (FX) movements are also likely to further play their part in depressing global trade. USD strength, predicated in more aggressive policy rate hikes and a better performing US economy, is a major drag to global trade growth. Around 40% of global trade flows are invoiced in USD and a stronger USD makes non-US imports more expensive. This further squeezes disposable incomes or even supports the substitution of imports for domestic products, negatively affecting trade volumes.

All in all, global trade volumes are set to decline substantially over the next months. Trade reflects the overall macro-economic environment and is just another indicator of the difficult environment that has been prevailing in recent months.