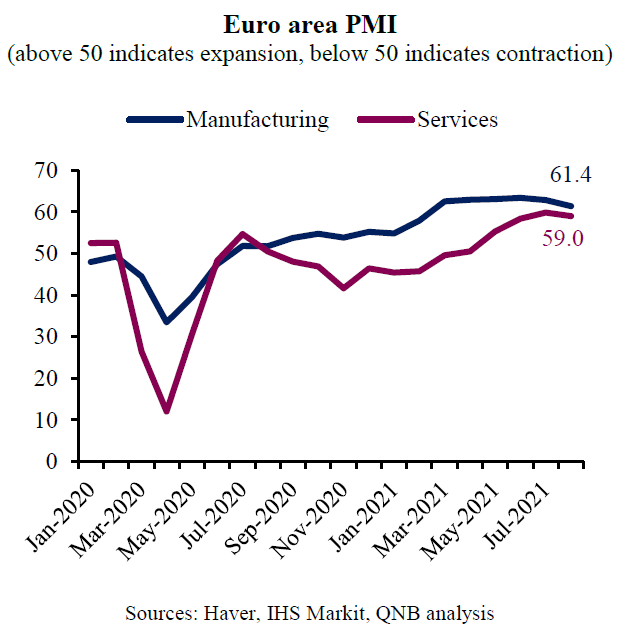

The Euro area composite PMI has recovered from its historic low in April 2020, caused by the outbreak of the Covid-19 pandemic. Continued progress with vaccination campaigns and lockdown restrictions have led to a visible decline in the number of infections. This has allowed governments to begin lifting restrictions with particular benefits for activities in the hospitality and retail sectors. The recovery has been supported by accommodative monetary and fiscal policy.

On the monetary side, the ECB continues to provide substantial monetary stimulus to maintain supportive financial conditions. On the fiscal side, besides normal fiscal policy support by individual member states, the Recovery Fund (RF), part of NextGenerationEU (NGEU), is intended to help repair the immediate economic and social damage produced by the pandemic. However, this picture of recovery masks important differences between the manufacturing and the services sectors. Our analysis elaborates on the recovery in the those two sectors in the Euro area.

The Purchasing Managers Index (PMI) is a survey-based indicator that measures whether various components of business activity have improved or deteriorated versus the previous month. A PMI reading of below 50 indicates that activity is contracting and above 50 indicates that activity is expanding. The PMI is usually split between manufacturing and services activities.

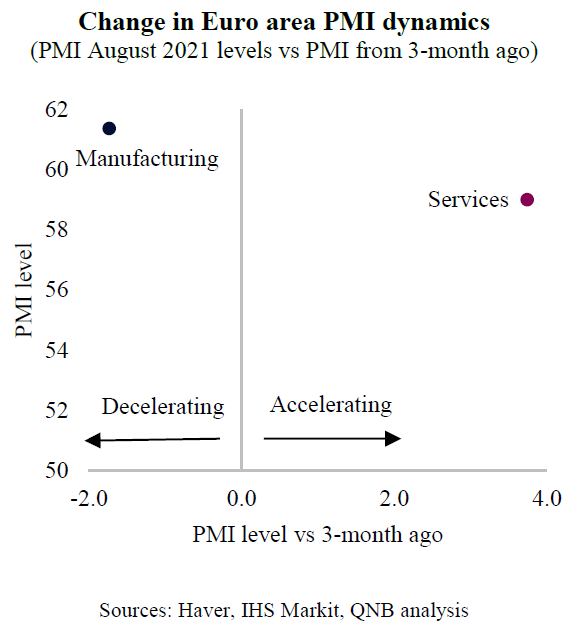

While the Euro area PMI remains strong, there has been a significant divergence in the direction of the two sectors over the last three months. The recovery of the manufacturing sector has been slowing while the services sector has been accelerating. Two factors explain this divergence.

First, Euro area manufacturing has been negatively affected by both the global economic slowdown and Covid-19 related supply constraints. The global slow down has been driven by fading fiscal stimulus in the US and headwind from the Covid-19 Delta variant in Asia. Weaker global demand slows manufacturing exports from the Euro area. In addition, Covid-19 related supply constraints, including transportation delays and material shortages, have been containing further manufacturing output growth in the Euro area.

Second, service sector growth has been supported by higher vaccination rates and the gradual reopening of several economies within the Euro area. After months of lockdowns and stringent social distancing measures, there was a build up of pent-up demand for outdoor activities and services. This includes a higher than normal desire from households to spend in activities, such as food servives and entertainment. Higher private consumption and government spending have also contributed to the acceleration of the services sector recovery in the Euro area.

All in all, the services sector in the Euro area has been accelerating, while the manufacturing sector has decelerated in recent months. Higher vaccination rates allowed for a substantial easing of lockdown restrictions, enabling for the reopening of the economy as well as domestic and international travel. Going forward, we expect Europe’s recovery to remain relatively strong for at least the rest of the year, as both monetary and fiscal policy are expected to remain supportive.

Download the PDF version of this weekly commentary in English or عربي