Vietnam is known as the land of the “Ascending Dragon” for its geographical shape and increasingly for its economic strength and resilience (See: Vietnam remains an Ascending Dragon despite COVID-19).

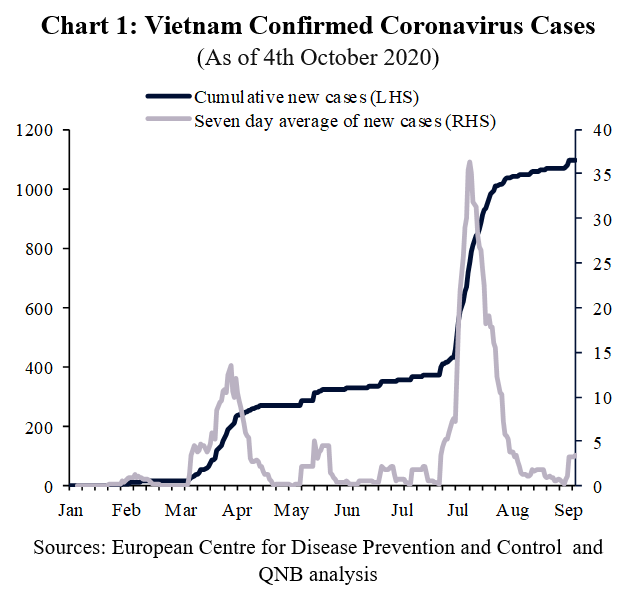

Early and efficient border closures and rigorous contact tracing allowed Vietnam to weather the first wave of the COVID-19 pandemic better than most. However, an outbreak in Danang city during the summer caused a second wave of infections (See Chart 1). Fortunately, the Vietnamese focus on contract tracing has enabled the authorities to bring the virus back under control with minimal disruption to the economy.

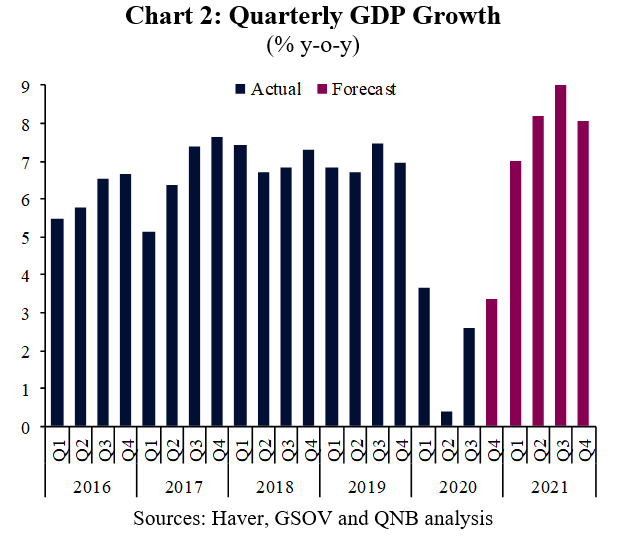

Official data for Q3 2020 shows GDP growing 2.6% year-on-year (y-o-y), which is even stronger than we expected earlier in the year (see Chart 2 below and our Economic Insight Report for our previous forecast). Vietnam’s strong recovery has been driven by three key factors: successfully containing the spread of Covid-19, resilient exports and support from fiscal and to a greater extent monetary policy.

First, strong and effective measures taken to control the spread of Covid-19

After almost 100 days without any community transmission, Vietnam faced a sudden outbreak in late July, originating in the city of Danang (Chart 1). The authorities swiftly enacted a lockdown of of the surrounding area and introduced social distancing measures across the country. This action had a modest negative impact on the retail and entertainment sectors. However, factories were kept open, which resulted in minimal disruption to the industrial sector. More importantly, the response was effective at controlling the outbreak, with fewer than four new cases per day recorded in September, down from a peak of over 50 a day in August.

Second, the strength and resilience of Vietnam’s exports sector

Exports reached a record level in August, despite the weakness of global demand. Strong demand for electronics has been important as electronics account for around 40% of Vietnam’s total exports. Demand for electronics has been boosted by employees working from home around the world, who need access to fast and reliable information technology. Vietnam has also seen exports to the US grow by 20% y-o-y in response to trade tensions between the US and China, as importers have shifted from China to alternative suppliers to avoid US tariffs. Vietnam is also benefiting from the free trade agreement with the EU that came into force in August.

Third, aggressive policy support, with the central bank doing the heavy-lifting

On the 1st October the State Bank of Vietnam (SBV) cut its policy interest rates by 50bps, bringing the cumulative easing of policy to 200bps since the start of the pandemic. With inflation subdued at just 3.9% y/y in September SBV has room to ease interest rates further in response to any negative shocks. In addition, the banking system is flushed with liquidity, which provides room for commercial banks to lower their interest rates further without the need for lower policy rates. On the fiscal side, Vietnam has seen a 25% y-o-y surge in state-level investment spending. However, a second stimulus package is likely to be limited to 1% of GDP (VND 60-70 Billion) in order to keep public debt below 60% of GDP.

We are upgrading our forecast for GDP grow to 2.9% this year, given the latest data for Q3 and the three factors discussed above. This would likely result in Vietnam being the best-performing economy in the region. Further spikes in new infections are a downside risk to the outlook, but the government’s track record, with effective containment measures, gives us confidence that they will continue to contain the virus with minimum disruption to the economy.

Download the PDF version of this weekly commentary in English or عربي