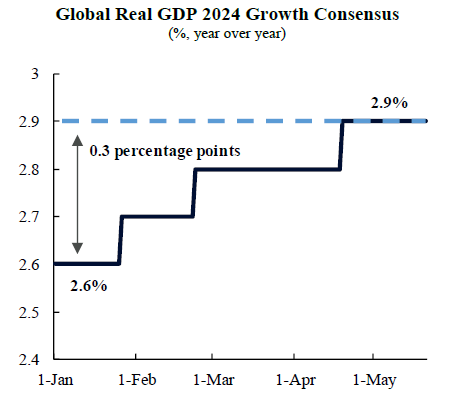

At the beginning of the year, strong headwinds set a pessimistic tone in outlining global growth expectations for 2024. The Bloomberg survey consensus is a useful tool that reveals the evolving views over major macroeconomic developments. This benchmark survey tracks forecasts from analysts, think tanks, and research houses. The Bloomberg survey showed that the expected pace of expansion in world GDP for this year was 2.6%. To put this number into perspective, it is one percentage point below the 3.6% average during 2000-2023. Furthermore, it is just marginally above the threshold of 2.5% below which a yearly growth rate indicates a global recession. During the period of 2000-2023, global recessions only occurred during the exceptional episodes of the Global Fincial Crisis, in 2009, and during the Covid pandemic, in 2020. Since 1980, the global economy has experienced four recessions according to this standard.

However, positive developments led to a revision of expectations in the three major world economies: the US, China, and the Euro Area, which jointly represent approximately 60% of global GDP. In this article, we examine the main reasons behind the improving outlook in the three major economies and their contributions to the global growth forecast.

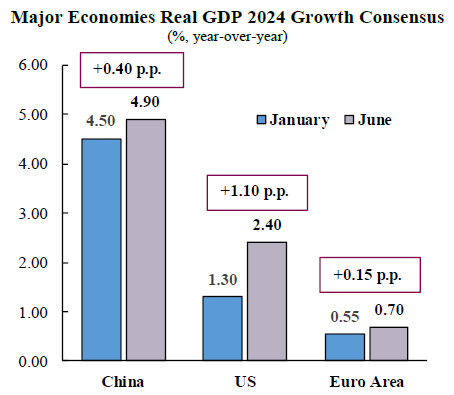

First, the performance of the US economy has bolstered a remarkable upward trajectory in its growth projections. The initial outlook reflected widespread pessimism amid still-high inflation rates that eroded the purchasing power of households, disruptive commodity markets, and the record monetary policy tightening by the Federal Reserve Board. With this backdrop, in January this year, the consensus for growth of the US economy in 2024 was a modest 1.3%.

However, data prints signalled that the economy was standing on firm footing. The GDP figures for the Q1-2024 showed that consumption of services, which accounts for a sizable share of the economy, grew at a outstanding annualized rate of 4%, significantly above the 2.3% pace of expansion in 2023. Overall, healthy household balance sheets and robust labour markets continue to provide support to consumption. Furthermore, leading indicators show that the anticipated deceleration of the US economy will be smooth. In fact, the current consensus points to growth of 2.4% for this year, just barely below the 2.5% growth of 2023. The improvement in perspectives for the world’s biggest economy provided a significant contribution to the improvement of the global outlook.

Second, China’s economic outlook has improved on the back of a robust recovery and new government stimulus measures. At the beginning of the year, pessimism surrounding China’s performance was one of the main reasons behind the relatively tepid global growth projections for 2024. The Bloomberg survey pointed to a growth rate of 4.5%, well bellow the pre-pandemic average of 6.7% between 2015 and 2019. Since then, data releases have surprised to the upside. Specifically, Q1-2024 delivered a year-on-year growth rate of 5.3%, beating expectations by a notable margin of 0.5 p.p.

Recently, the Chinese government has put into action a battery of policy measures to provide support to the private sector and further promote foreign direct investments. These initiatives range from interest rate reductions and liquidity injections to public investment. Furthermore, the government addressed concerns surrounding the real estate sector, providing financial aid to developers and government backed firms, and incentives for regional developers to purchase unsold homes and allocate them to low income residents. Given the improvement in momentum and policy stimulus measures, we believe that there is room for further positive revisions in China GDP growth.

Third, after an extended period of stagnation, the Euro Area is undergoing a mild recovery that backs positive revisions of growth forecasts for 2024. Since early 2022, the Euro Area has been in a negative spiral, facing significant headwinds from high energy prices, geopolitical uncertainty, and weak external demand. Growth was -0.1% in Q2 and Q3 of 2023, implying the bloc registered a technical recession, before stalling in Q4. At the beginning of this year, the consensus growth forecast for the bloc for 2024 stood at a modest 0.55%.

A recovery started to gain traction in Q1-2024, with GDP expanding 0.3% over the previous quarter, providing a justification to revise expectations. Even if looming headwinds don’t allow for excessive optimism, several factors provide confidence to upgrade growth forecasts. The combination of falling inflation with high wage growth implies gains in the purchasing power of households, which will likely translate into firmer spending. Additionally, with the end of the “global manufacturing recession,” manufacturing activity is expected to become more supportive for Euro Area growth over the coming quarters. Finally, the beginning of a policy rate reduction cycle by the European Central Bank (ECB) will provide further backing to the economy. On the back of these positive developments, consensus growth expectations for the Euro Area have improved, even if dimly, to 0.70% for 2024.

All in all, the outook for the global economy for this year has improved on the back of positive developments in all the three major economies (the US, the Euro Area, and China). Although the expected pace of expansion of 2.9% is below the long-term average, it stands at a safe distance from the recessionary range.

Download the PDF version of this weekly commentary in English or عربي