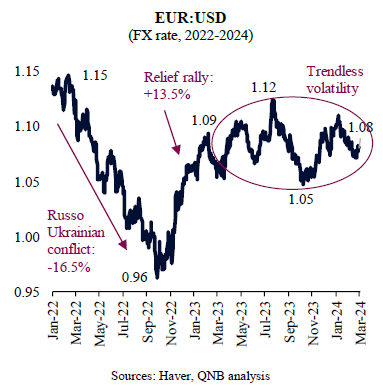

The Euro (EUR) has experienced significant volatility since the beginning of the Russo-Ukrainian conflict in late February 2022, when deeper concerns about the overall health of the Euro area economy emerged. Initially, as pessimism about the escalation of the conflict and European energy security took hold, the EUR depreciated sharply against the USD, finding a bottom below the parity level. However, in late 2022, as the scope of the conflict in Eastern Europe became contained and the Euro area was able to avoid the more dire consequences of an energy crisis, the EUR rallied significantly, recovering most of the previous losses. Thereafter, the EUR has been presenting some trendless volatility.

As investors and analysts debate whether the most important currency pair will break its current wide range (EUR:USD 1.05-1.12) to the upside (EUR appreciation) or to the downside (EUR depreciation), the general outlook for the Euro area remains negative. While the Euro area as a whole was able to avoid a recession in recent quarters, there is little room to be overly optimistic about growth in the region. This is because the 450 basis points (bps) in interest rate hikes by the European Central Bank (ECB) since July 2022 still needs to pass through to the rest of the real economy, affecting investment and consumption decisions. Moreover, after more than a year supporting households and corporates from the negative effects of higher energy and food prices, fiscal authorities are set to gradually withdraw emergency stimulus. This is negative for the growth outlook and, therefore, for the EUR, as FX movements are dominated by changes in expectations for growth and real interest rate differentials.

In our view, however, there is limited downside for the EUR in 2024. Indeed, we even see some scope for EUR appreciation in the coming quarters. Two arguments support our view.

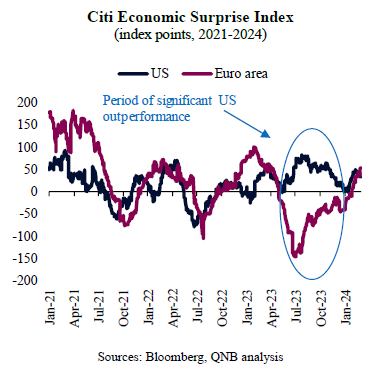

First, relative growth expectations between the US and the Euro area are likely to favour the Euro area over the coming months, after a long period of US outperformance. The flurry of negative economic data surprises in the Euro area seems to have exhausted itself, pointing to some extreme pessimism that is already producing positive surprises. This is reflected by the recent moves in the Citi Economic Surprise Index, a timely figure that measures the pace at which economic indicators are coming in above or below consensus forecasts. For the first time in nearly a year, data has been mostly producing positive surprises in the Euro area. In contrast, positive surprises have been weakening in the US. As a result, the existing “growth gap” between the US and the Euro area is expected to narrow significantly, supporting the EUR in the process.

Second, lower and falling inflation in both the Euro area and the US is likely to produce movements in interest rate differentials that favour the EUR against the USD. The US Federal Reserve (Fed) has so far presented a more aggressive agenda for interest rate cuts in 2024 than the ECB. Hence, as the Fed is expected to cut rates by 100 basis points (bps) this year, the ECB is expected to cut only 75 bps over the same period, even if inflation in the Euro area is slowing down more rapidly than in the US. This will take US nominal rates from 5.5% to 4.5% and Euro area rates from 4% to 3.25%, narrowing the interest rate differential from 150 bps to 125 bps. This favours the EUR, as a lower yield differential will push more global capital towards the Euro area versus the US.

All in all, revisions in relative growth expectations and rate differentials are likely to favour the EUR versus the USD. This should limit a more significant downside for the EUR and should place the currency in the upper part of its recent rage, with the EUR:USD rate expected around 1.10-1.15.

Download the PDF version of this weekly commentary in English or عربي