Few indicators convey as much information about global macro trends than the direction of currency fluctuations. This is particularly valid when it comes to deep, liquid foreign exchange (FX) markets of major currencies from advanced economies, such as the US Dollar (USD), the Euro (EUR), the Japanese Yen (JPY), the Swiss Franc (CHF) and the Pound Sterling (GBP). FX is driven by capital flows, which corresponds to real time reactions to expectations about risk appetite, relative economic performance and interest rate differentials.

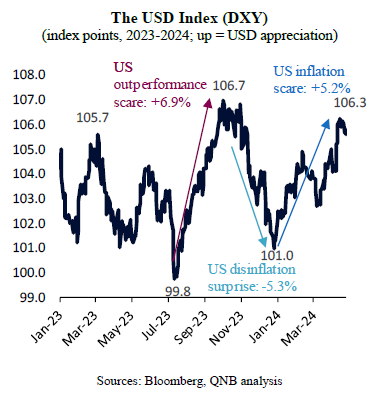

In recent months, major FX markets have presented significant volatility. In fact, the USD Index (DXY), a traditional benchmark that measures the value of the USD against a weighted basket of six major currencies, has experience marked fluctuation on the back of macro cross currents. In Q3 last year, amid a significant economic re-acceleration and US outperformance, the DXY appreciated by almost 7% against the July 2023 lows. Shortly after this, however, positive US disinflationary surprises led to a “dovish” pivot from a US Federal Reserve (Fed) promising rate cuts, which led to a rapid depreciation of the DXY to the lows of late December 2023. This movement was later almost entirely reverted by an unexpected re-acceleration of inflation.

As the DXY approaches the critical levels seen in September 2023, amid “peak” Fed hawkishness, analysts and investors debate the direction of the USD. Many believe that the USD should be well supported by a robust US economy and a Fed that could be forced to act more “hawkish” than its peers, due to higher US inflation. In our view, however, there is scope for a significant USD depreciation. Three factors support our view.

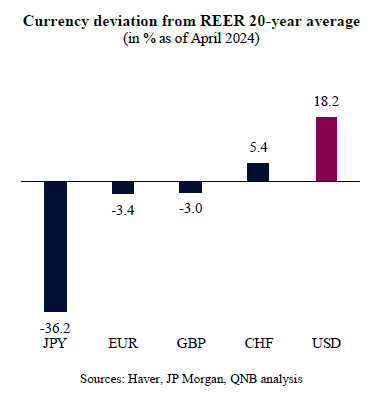

First, an assessment of the USD suggests that the currency is overvalued and in need for an adjustment. A common way to look at currency “valuations” is to analyse trade-weighted, inflation-adjusted exchange rates, i.e., the real effective exchange rates (REER), and compare it to their own long-term averages or historical norms. This REER metric is more robust than traditional FX rates as it captures changes in trade patterns between countries as well as economic imbalances in the form of inflation and inflation differentials. The REER picture for April 2024 suggests that the USD is indeed the most overvalued currency in the advanced world, by more than 18% of its notional “fair value.”

Second, relative growth expectations between the US and the rest of the world are likely to favour the rest of the world over the coming months, after a long period of US outperformance. The flurry of negative economic surprises in the Euro area and Asia seems to have exhausted itself, pointing to some extreme pessimism that is already producing positive surprises. This is expected to be further accelerated by the ongoing global manufacturing recovery. After two years of a deep “recession,” the global manufacturing cycle is turning around in a movement that should benefit more the “factory heavy” economies of Europe and Asia. As a result, the existing “growth gap” between the US and the rest of the world could narrow significantly more than previously expected, leading to a depreciation of the USD.

Third, despite the existing uncertainty about the path of US policy rates, we believe that rate cuts are going to be enacted by the Fed in H2 2024. While the recent US “inflation scare” is affecting expectations about the next Fed policy moves, a more comprehensive look at leading inflation indicators suggest that there is no room for panic. A meaningful downtrend in non-cyclical inflation and a weakening labour market favour further price normalization over the coming months. The Fed should then cut rates, as current policy rates are too high for both the existing and expected level of inflation. This will ease global financial conditions, allowing for other central banks to also cut rates without undue pressures in their currencies. Hence, US real rates are currently at a level that justifies rate cuts, which would then narrow the interest rate differentials with other economies, without impacting the Fed mandate of 2% inflation.

All in all, we believe that there is little room for further USD appreciation much beyond the existing levels. The US currency is expected to adjust to more “fair levels,” which should be supported by a narrower growth gap between the US and the rest of the world as well as the beginning of the US easing cycle later this year.

Download the PDF version of this weekly commentary in

English

or

عربي