More than two years since Covid-19 was first discovered, the global economy is shrugging off a new wave of the pandemic. Over the past two years the Covid-19 virus has mutated and evolved through a number of variants of concern (VOC), with the latest being Omicron. Humanity’s response to the pandemic has also evolved through several stages from hard lockdowns through to the development of effective vaccines, re-opening and more focused restrictions. The evolution of the virus and initial lockdowns led first to the largest globally synchronised recession since world war two in early 2020. Then, subsequent waves of the pandemic have acted as headwinds to the global economic recovery of declining intensity.

Our analysis explains why Omicron acts as headwind for the global economy and why we expect the headwind to be both limited and temporary.

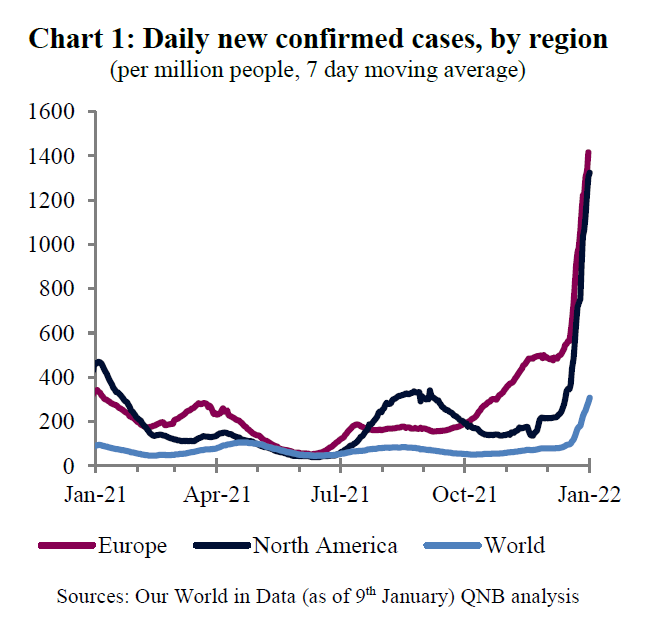

First, Omicron is more contagious than earlier VOCs and has led to a massive surge in cases of Covid-19 (Chart 1). With 36 mutations in the spike protein, Omicron is approximately two to three times more transmissible than the Delta variant. In addition, Omicron’s mutations also mean that antibodies from a previous infection, or vaccines developed to target the original virus, are much less effective. For example, the protection from two doses of the Pfizer-BioNTech vaccine against any symptomatic infection is estimated to have dipped below 40 percent. Indeed, it is fair to say that vaccines have been unable to prevent mild infections and transmission of the Omicron variant.

Second, Omicron has already hit the core of the global economy. Omicron arrived in Europe and North America at the same time as the festive season encouraged travel and large indoor gatherings. Consequently, those regions have seen the largest surge in cases so far and countries have needed to tighten restrictions to avoid over-loading their healthcare systems (Chart 1).

These two regions account for the lion’s share (53%) of global GDP and have large consumer services sectors, which are most vulnerable to government restrictions, lockdowns, or people simply choosing to stay at home.

In summary, we expect a negative hit to global economic activity beginning in Q4 2021 and continuing into Q1 2022, because Omicron is so contagious and has hit the core of the global economy. Now we turn to why we expect the economic headwind from Omicron to be both limited and temporary.

In summary, we expect a negative hit to global economic activity beginning in Q4 2021 and continuing into Q1 2022, because Omicron is so contagious and has hit the core of the global economy. Now we turn to why we expect the economic headwind from Omicron to be both limited and temporary.

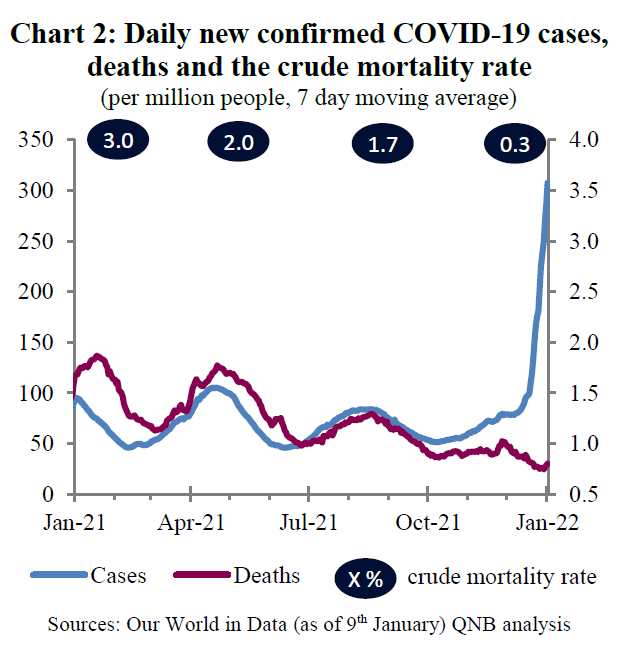

Omicron is proving to be less severe than other VOCs and there is clear evidence that vaccines remain effective at reducing the severity of infection. This can be seen by the crude mortality rate (reported deaths per reported case) falling to only 0.3% at the time of writing, down from 3% in early 2021 (Chart 2). Indeed, studies show that the protection from two doses of the Pfizer-BioNTech vaccine against severe illness remains robust at 70 percent. Further, people who have also received boosters are even better protected from severe disease.

Governments have therefore tightened restrictions in a more targeted way than during previous waves of the pandemic. In addition, restrictions should also only be necessary for a short period of time as governments and populations become more tolerant of higher case numbers due to the reduced severity and lower mortality rate. We also expect the build-up of natural immunity, in addition to continued vaccination campaigns, to help to reduce the number of new cases, even as restrictions are lifted later in the year. We therefore expect restrictions to soon begin to be relaxed, providing a boost to economic activity in the second half of 2022.

As a result, we expect the IMF to downgrade their estimate of global GDP growth in 2021 and their projections for 2022 in the forthcoming January update of their World Economic Outlook. However, we anticipate only modest downward revisions in both years; the impact of Omicron on comes only at the end of 2021 and the negative impact at the beginning of 2022 will be partially offset by stronger activity later in the year.

Download the PDF version of this weekly commentary in English or عربي