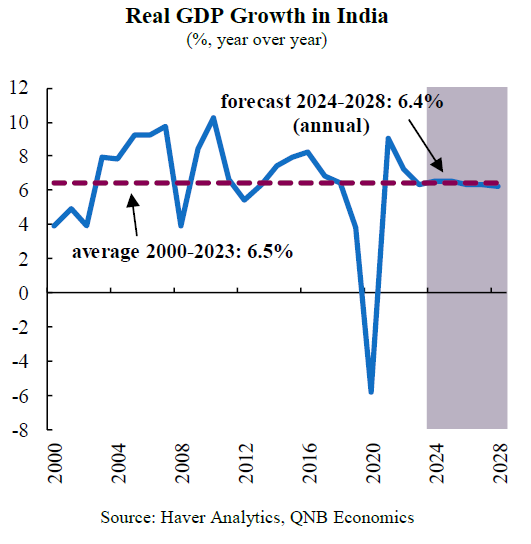

India is one of the fastest growing economies in the world, and rapidly transforming into an engine of global growth. During the 2000-2023, which includes the volatile years of the Global Financial Crisis and the Covid-pandemic, the average growth rate for the South-Asian giant was 6.5%. This sustained performance pushed India to become the sixth economy in the world, representing 8% of the global economy. Given its size, a 6.5% growth rate for India adds 0.52 percentage points (p.p.) to global growth. This implies that India explains an important share of the 3.2% global growth expected in 2024.

India has been able to achieve this performance in spite of significant structural obstacles. Firms and international institutions have pointed to excessive regulation and a burdensome bureaucracy, disproportionate trade and labor market restrictions, and high transaction costs. Even with these difficulties, India’s strong growth momentum is expected to continue, and contribute to bring a large share of its population to higher standards of living. In 2000, GDP per capita was USD 442, and reached USD 2,500 in 2023, within the lower middle income range according to the classification of the World Bank. In approximately one more decade, the country could surpass the threshold of upper middle income country of USD 4,465, almost 10-fold the per capita level two decades before.

India is expected to maintain its firm growth trayectory and continue to be one of fastest expanding economies, with rates of 6.4% in the next several years. In this article we discuss the 3 key factors that will support India’s growth in the coming years.

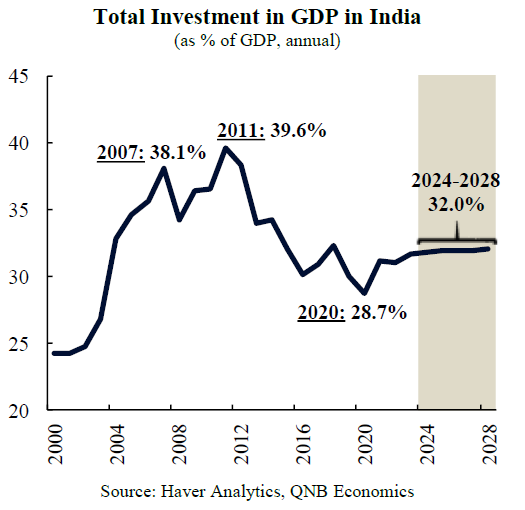

First, high investment levels will boost aggregate demand and expand production capacity. As a share of GDP, investment has recovered from the low reached in the aftermath of the Global Financial Crisis and during the Covid-pandemic, and is expected to remain above 30% in the medium term. An important part of this story is explained by the impulse given by the central and state governments to capital expenditures.

The central government’s budget for infrastructure has more than tripled from five years ago to USD 135 billion for the 2025 fiscal year. This figure is almost double if state-level spending is included. Infrastructure investment has a significant impact in a country with substantial needs, and will deliver a much-needed improvement of railroads, highways, electricity networks, and waterways, among other crucial infrastructure. The number of airports, for example, is expected to increase from 148 a few years ago, to 200 by next year, which is accompanying a sizable growth in airline services. In addition to reducing logistical and transportation costs, capital expenditures by the government will encourage business investment. In fact, public investment is known to have the highest multiplier on economic activity, and to be effective in incentivising private companies to invest.

Second, a large, young, and growing population will provide a seemingly endless supply of labor to bolster the expanding economy. Recently, India overtook China as the most populous country in the world, after reaching 1.4 billion people. With a median age of 28 compared to 39 in China, the problem of an aging population that is becoming widespread in other countries, is distant in this South-Asian nation. Additionally, the participation rate of the labor force is only 51%, which is 25 p.p. below that of China. To a large extent this difference is explained by the exceptionally low participation rate of women in India at 25%, which is a significant 46 p.p. lower than in China. These statistics underlie the considerable potential and the encouraging trends in increasing labor supply, which will continue to support the economic growth trajectory of India.

Third, an extensive reform agenda is set to provide firm support to growth in productivity. Unlike other emerging economies in recent years, improvements in productivity have been an important factor in explaining economic growth in India. The liberalisation of labor laws, which have already been promoted in many Indian states, will contribute to a rebalancing of workers out of agriculture towards more productive sectors. According to the IMF, labor productivity in agriculture is a mere 2.3% of that of the world’s most productive agricultural industries. Labor productivity in services in India is 18% relative to the highest productivity service workers. Given that 46% of the Indian labor force is in the low-productivity agricultural sector, encouraging the transition of workers to more productive activities will provide a significant boost to the economy.

The government is also making progress in negotiating new bilateral trade agreements, and removing tariff and non-tariff barriers to trade. This will expose Indian producers to a healthy degree of competition, and help them increase productivity. Reforms have already attracted larger investments in manufacturing and technology from multinational firms such as Apple, Samsung, and Boeing. Going forward, the ongoing reform process will continue to play a leading role in India’s growth story.

All in all, India is set to continue on a firm growth path, expanding at rates close to 6.5% in 2024 and 2025, and maintaining strong momentum afterwards on the back of across-the-board contributions from capital, labor, and productivity.

Download the PDF version of this weekly commentary in

English

or

عربي