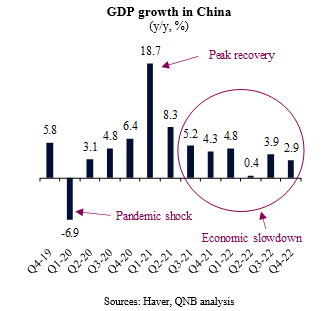

China, a pivotal economic force accounting for approximately 40% of global GDP growth since the Global Financial Crisis (GFC), has navigated a series of significant fluctuations in recent years. In the wake of the initial Covid-19 outbreak in Q1 2020, the country achieved an impressive 18.7% GDP growth at its peak recovery, maintaining positive momentum from mid-2020 to mid-2021. During this period, China stood as the first and only major economy to exhibit positive GDP growth in 2020.

However, a combination of domestic factors has since led to a pronounced economic slowdown in China. The implementation of the Zero Covid policy, marked by lockdowns in tier-1 cities, restrictive bank lending practices towards the overleveraged real estate sector, and aggressive regulatory clampdowns across various industries, culminated in stagnant Q2 2022 real GDP growth and the country's worst economic performance in decades. Moreover, the anticipated recovery in the second half of 2022 failed to materialize due to new Covid-19 outbreaks and subsequent lockdowns across the nation late last year.

Expectations for growth in China in 2023 have become more positive due to the reversal of key cyclical headwinds. The nation is shifting away from Zero Covid policies, reopening and normalizing its economy. Additionally, China is moving towards a more supportive macroeconomic policy stance, easing credit conditions for the real estate sector, and reducing regulatory uncertainties in key technological industries. These policy changes collectively painted a brighter outlook for China's economic growth in 2023, with a consensus that GDP would re-accelerate this year.

Several months into the year, how is activity in China stacking vis-à-vis expectations so far? In our view, China’s economic activity appears to be tracking in line with the more optimistic expectations. Three main factors substantiate our analysis.

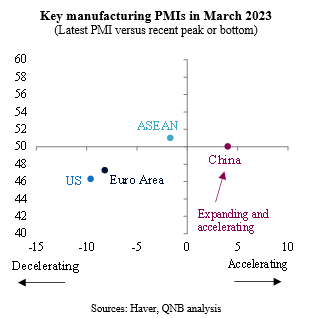

First, leading indicators of activity in China are already pointing to a more significant recovery. The manufacturing Purchasing Managers’ Index (PMI) of China, a survey-based indicator that measures whether several components of activity improved or deteriorated versus the previous month, seemingly bottomed last year. Traditionally, an index reading of 50 serves as a threshold to separate contractionary (below 50) from expansionary (above 50) changes in business conditions. This higher frequency indicator is not only pointing to a positive crossing into expansionary territory but also to a significant acceleration in manufacturing activity, despite a marked slowdown in global growth. In contrast to China, activity is slowing down or even contracting in other major economies, such as the US, the Euro area, and the emerging market economies in Southeast Asia (ASEAN).

Second, the economic re-opening appears to be in full swing, which is a powerful tailwind to the battered service sector in China. Data shows that traffic congestion remains elevated and above 2021-22 levels, with subway passenger volume experiencing strikingly high year-over-year growth. The demand for oil has recovered to above pre-pandemic levels, and the implied oil demand from scheduled domestic flights is particularly high. Consumption during the Chinese New Year holidays suggests a robust initial recovery, with high-end and mid-to-high-end discretionary service sectors outperforming. Offline consumer service sectors, such as tourism, movies, and catering, saw a strong rebound in demand during the Spring Festival holidays. With spending from domestic tourist trips and recovering, and box office theatre revenue reaching the second highest take on record, the extent of pent-up demand release for offline discretionary consumer services have been exceeding expectations so far.

Third, Chinese authorities continue to pivot away from open-ended regulatory changes in key technological sectors. Over the last several quarters, comprehensive regulatory reviews in certain industries, such as private education, fin-tech, e-commerce, food delivery and ride hailing, created severe business uncertainty, partially preventing new investments and even innovation in related activities. In recent months, however, authorities started to conclude their regulatory reviews, providing clearer guidance for businesses and issuing more formal licenses to operate to important corporates that were previously operating under “grey areas.” This has been lessening business uncertainty and is already supporting a pickup in private sector investments and innovation.

All in all, the Chinese economy appears to be on track for a solid recovery in 2023, driven by a confluence of favourable factors. The manufacturing sector is showing signs of expansion, while the service sector is benefiting from the economic reopening and pent-up consumer demand. Furthermore, regulatory clarity in key technological sectors is reducing business uncertainty and fostering private sector investments and innovation. Despite market scepticism about a more prolonged and powerful Chinese recovery, we expect China’s growth to surprise to the upside.

Download the PDF version of this weekly commentary in English or عربي