Commodities are one of the cornerstones of the global economy, vital for powering construction projects, fuelling vehicles, and providing essential resources and sustenance to households. Hence, it is not a surprise that fluctuations in commodity prices reflect the ongoing dynamics of key industries, providing critical insights into the overall health of the global economy. This includes relevant information for trends on sentiment and inflation, often leading or confirming cyclical turning points.

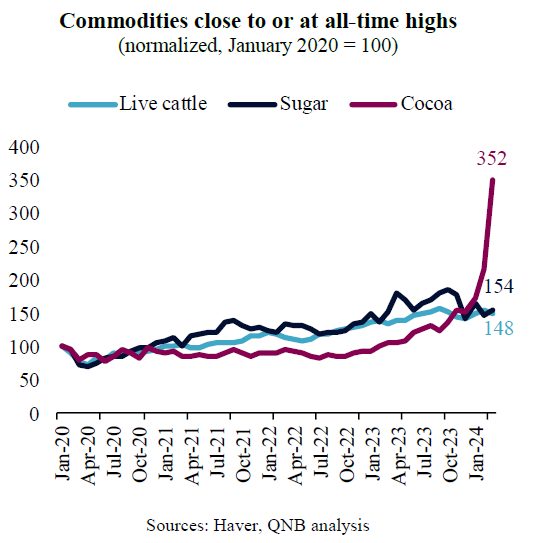

This is why the recent surge in prices for certain commodities, such as cocoa, sugar and live cattle, caught the attention of economists and investors alike. Are these price surges a sign of things to come? Are those commodities foretelling a re-acceleration of economic activity and inflation over the coming months?

In our view, there is no reason to read too much into the movement of singular commodities. They often reflect idiosyncratic factors associated with those particular markets, including weather patterns or disruptions in major producers, rather than major macro movements. If anything, prices within the overall commodity complex seem to sustain the benign macro view of a “soft landing” with a further moderation of inflation. Three factors support this position.

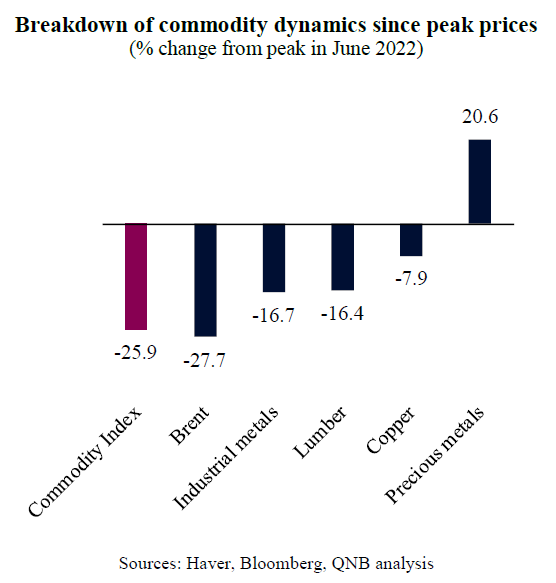

First, broader commodity prices are still significantly below their recent peak in May 2022, seemingly challenging the narrative of a global economic re-acceleration or inflation pick-up. This is also expressed in the more pronounced correction of highly cyclical commodities, such as energy, base metals and construction related materials. Within energy, Brent crude oil prices, while still above pre-pandemic levels, are down 27.7% from their recent peak. Within base metals and construction related materials, copper and lumber prices, important proxies for activity in China and the US, have also declined significantly from their recent peaks. Such price performance suggests that the global growth outlook is still dominated by headwinds, and that inflationary pressures are unlikely to mount again.

Second, precious metals are also pointing to a weak global economy. Gold prices are at all-time highs, up 25% since June 2022 to close to USD 2,300/troy oz. However, silver prices, key as an input for the new economy (technology and clean energy industries), are significantly below its recent highs. A rising gold-to-silver ratio amid a strong gold performance is a sign that deflationary pressures are taking hold with no pressure from overall demand or economic activity.

Third, the combination of robust gold prices with flat to lower 10-year US Treasury yields in recent quarters suggests that investors are now more inclined to think that uncertainty is heightened and the upside for global growth is limited. While gold seems to have de-coupled from inflation trends since the pandemic, it is still a traditional safe-haven asset to hold in times of uncertainty and negative macro developments. Higher safe-haven demand in macro-driven asset classes tend to be correlated to periods of slowing growth and inflation.

All in all, idiosyncratic moves in certain commodities do not reflect the overall macro message of the segment as an asset class. The more macro sensitive components of the commodity complex are conveying a signal of slowing growth and moderating inflation, consistent with the dominant narrative of a “soft landing.”

Download the PDF version of this weekly commentary in English or عربي